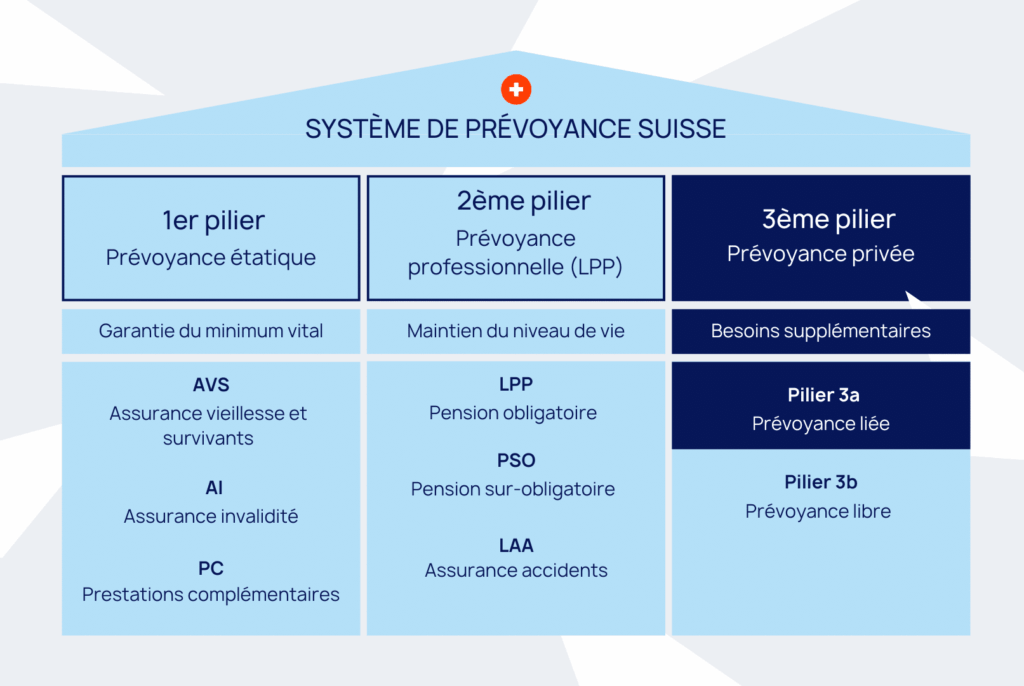

Diagram: The role of Pillar 3a in the Swiss pension system

Introduced in 1972 in the Constitution, pillar 3a represents tied individual pension provision. It is characterized by its favorable tax framework and has the main purpose of preparing for retirement. This private pension represents a voluntary savings that complements the first two pillars (AHV and occupational pension) and, in exchange for tax deductions, comes with restrictions on withdrawals. The accumulated funds can only be accessed in the event of retirement, disability, death, or for the purchase of a first home, under certain conditions.

In 2026, it will be possible to pay out the following following amounts in individual linked provision:

Anyone engaged in gainful employment subject to AHV in Switzerland can open a pillar 3a. This includes employees, self-employed individuals, recipients of unemployment benefits, and cross-border workers.

Contributions paid are deductible from taxable income at the federal level, which helps reduce annual taxation. In addition, upon withdrawal, the capital is taxed at a reduced rate, at 1/5 of the regular tax.

Furthermore, during the term of the contract, no wealth tax will be levied, allowing capital to grow without additional costs.

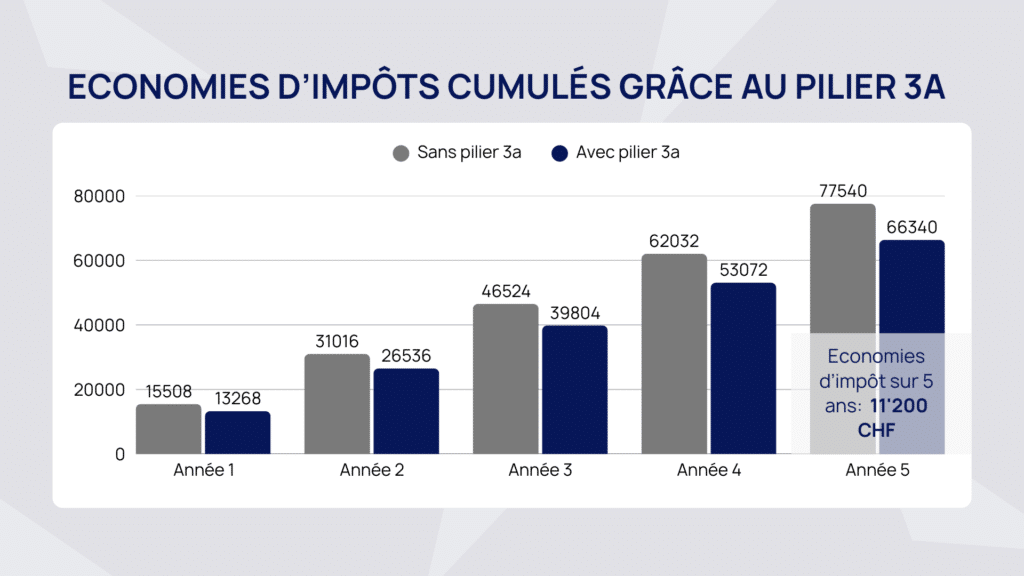

Chart: Cumulative tax savings from Pillar 3a contributions

Over one year, you could potentially save 2,240 CHF in taxes. Over five years, this would amount to approximately 11,200 CHF in taxes saved.

Scenario: single person living in Geneva with a gross income of CHF 100,000.

To calculate your tax deduction, you need to know your marginal tax rate. Let's take an example:

After applying these rates and the canton's progressive tax scale, we obtain:

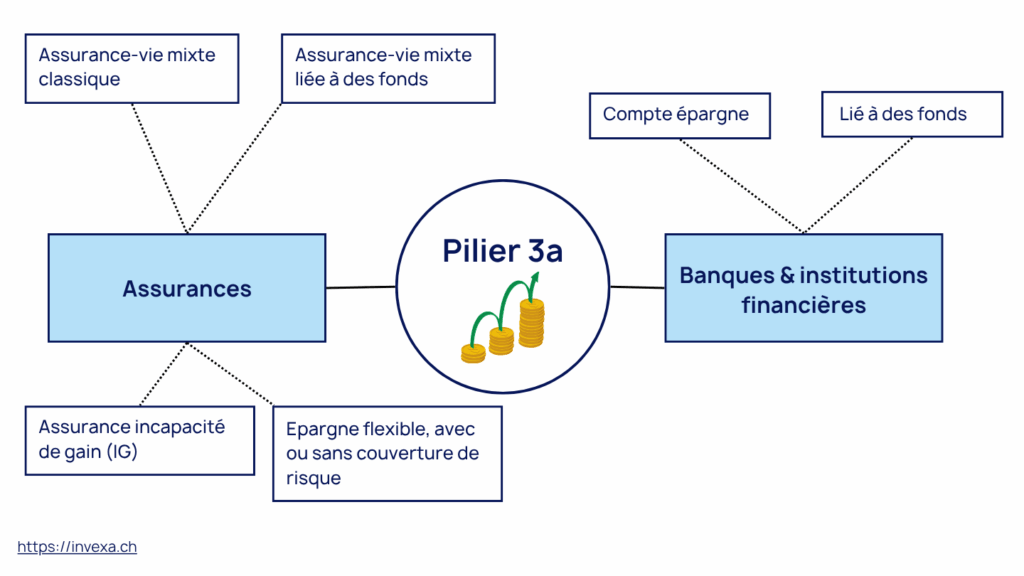

There is a wide range of options within tied pension provision. We generally distinguish between two main categories: Pillar 3a with a bank and Pillar 3a with an insurance company.

| Criteria | 3A insurance | 3A bank |

|---|---|---|

| Payment frequency | Determined in advance | Flexible |

| Type of investment |

|

|

| Surplus earnings | Profit sharing | No profit sharing |

| Possible coverage |

|

No |

| Bankruptcy guarantee | Amount guaranteed to 100% | Guaranteed amount up to CHF 100,000 |

| Waiver of premiums in the event of disability | Possible | No |

| Investment horizon | Long-term only | Medium to short term |

| Share of guaranteed capital | Possible | No |

| Pledging | Possible | Possible |

| Key benefits |

|

|

Diagram: Pillar 3a banking and insurance investment opportunities

A good 3a fund-linked insurance is usually less expensive than a bank-based pillar 3a in the long term. However, in insurance, fees are charged at the beginning of the contract. This is a factor that must be considered in case of an early withdrawal.

The early withdrawal conditions of pillar 3a are strictly regulated to ensure that the savings remain dedicated to pension provision and retirement. Here is a breakdown of the different situations in which an early withdrawal is possible, either partially or in full:

Retirement benefits can be paid out as early as 5 years before the insured person reaches the standard OASI retirement age (“reference age”), and at the latest five years after.

Advance withdrawal is permitted when Pillar 3a savings are used to buy back contributions in a 2nd pillar pension scheme. This option enables you to top up or regularize your occupational pension capital in the event of retirement.

If the client receives a full disability pension from the DI and the risk of disability is not covered by the pension plan, the early withdrawal can be activated.

Early withdrawal is also possible for the policyholder who changes to a new self-employed activity. This allows access to the necessary liquidity to support their professional transition.

If the pension fund member sets up their own business, they can apply for early withdrawal. The aim is to provide financial support when starting a self-employed or entrepreneurial activity, which is often crucial in the early stages of setting up a business.

If the policyholder permanently leaves Switzerland, they may make an early withdrawal of their funds. This provision is intended to allow the insured person to access their savings when settling abroad.

Early withdrawal is also possible when the funds are used to purchase a home for one's own needs or to repay mortgage loans. This condition facilitates home ownership by allowing insured persons to use their savings in a practical way for a real estate project.

There is no legal limit to the number of 3a accounts you can hold. In practice, you may open several accounts — for example, a bank account and a life insurance policy.

However, the annual contribution ceiling remains the same and applies to the total of all your payments, which means that the total amount deposited cannot exceed the ceiling set by law.

On the other hand, the surviving spouse or registered partner remains priority as long as the law has not changed. It should be noted that Parliament and the Federal Council are currently reviewing a reform of OPP 3 which should offer more flexibility in the designation of beneficiaries starting in 2027, notably the possibility of prioritizing children even in the presence of a spouse.

However, the surviving spouse or registered partner remains priority as long as the law has not changed. It should be noted that Parliament and the Federal Council are currently reviewing a OPP 3 reform which is expected to provide more flexibility in the designation of beneficiaries starting in 2027, including the possibility of favoring children even in the presence of a spouse.

Withdrawal under the Home Ownership Promotion (EPL) allows you to withdraw all or part of your 3a capital to finance your primary residence.

The pledging of the 3rd pillar involves using your contract as collateral with the bank, without withdrawing the money.

The choice mainly depends on current mortgage rates and your tax burden. If rates are low, pledging is often mathematically superior. If you want to minimize your monthly expenses as much as possible, withdrawal is more appropriate.

It is also possible to combine the two. For example, withdraw a portion to reach 20% of equity and pledge the remainder to guarantee the indirect amortization of your loan.

Starting in 2025, pillar 3a allows you to buy back unpaid contributions from previous years, offering an opportunity for tax optimization and retirement planning.

The first buy-backs will be possible from 2026 to cover gaps from 2025, with a maximum retroactive period of 10 years. The annual maximum buy-back amount is 7,258 CHF (for employees and self-employed), fully deductible from taxable income.

The conditions include income subject to social security contributions and payment of the full annual contribution. This measure is in addition to the options for transferring to the 2nd pillar and is a strategic tool for increasing one's retirement savings while reducing taxes.

Two variants exist in the 3rd pillar (private pension). Pillar 3a is a tied retirement savings, offering significant tax deductions. The funds are locked and can only be withdrawn in specific events (retirement, home purchase, disability, or permanent departure from Switzerland).

The pillar 3balso known as unrestricted pension planis, for its part, a additional savings more flexible, with no strict constraints on use. Although it benefits from fewer tax advantages when taken out as insurance, it allows funds to be used freely for a variety of projects. In short, making the difference between a 3a and a 3b flexibility and tax deductions to exploit.

Contrary to popular belief, pillar 3a is not reserved for holders of a C permit or for Swiss citizens. However, for individuals taxed at source (B or L permit holders, or cross-border workers), the tax advantage is not automatic and requires proactive action.

If you are taxed at source and earn less than CHF 120,000 a year, your 3a deductions are not taken into account in your monthly scale.

The solution: You must request Ordinary Subsequent Taxation (TOU) before March 31 of the following year.

Once claimed, the TOU is irreversible for subsequent years. It's crucial to check whether your other deductions (travel expenses, meals, etc.) offset any worldwide income or wealth that could increase your tax liability.

For cross-border workers, pillar 3a remains an excellent pension tool, but its tax benefit depends on your quasi-resident status (Geneva).

Remember that it is now possible to make retroactive buy-backs to fill in gaps in your contributions from previous years (under certain conditions). This opportunity is also available to “sourciers” through the TOU procedure.

Choosing the best Pillar 3a in Switzerland depends on your profile, age and pension needs. To help you quickly identify which solution best suits your situation, we've created a comprehensive matrix with detailed explanations for each profile.

| Profile | Recommended solution | Protection to include | Priority |

|---|---|---|---|

| Single employee < 40 years old | 3a Insurance + 3a Bank (funds) | Disability due to illness | Protection + Performance |

| Family with children | Priority 3a insurance + 3a Bank (funds or guaranteed capital) | Death + Sickness disability | Family protection |

| Self-employed without BVG | Assurance 3a (funds) | Death + Sickness and accident disability | Protection + Taxation |

| Cross-border commuter (quasi-resident) | Bank 3a (funds or interest-bearing account depending on horizon) | Impossible in Switzerland | Flexibility + Taxation |

| Near retirement < 10 years | Bank 3a only (interest-bearing account or low % shares) | Too expensive | Capital preservation |

In practice, there is no universal solution when it comes to pillar 3a. The choice mainly depends on age, family situation, professional status, and investment horizon. A combination of multiple banking and insurance solutions often allows for optimizing flexibility, protection, and tax advantages simultaneously.

A personalized analysis is essential to adapt your pension strategy to your actual needs, and to avoid making inappropriate decisions over the long term.

Are you unsure between several providers? We help you choose the most suitable 3a solution.

Find out how much you can potentially save between now and retirement with a pillar 3a solution.

Past or simulated performance is no guarantee of future performance. This projection is provided for information purposes only.

Opening a 3a pillar is an important decision that deserves careful analysis. It is essential to define your profile and needs before selecting and comparing the various solutions available. The fees and conditions can vary significantly from one provider to another, which can have a major impact on your long-term returns.

Pillar 3a is a form of tied individual pension provision in Switzerland. It allows you to save for retirement while benefiting from tax advantages. It is subject to strict conditions regarding beneficiaries, amounts paid in, and withdrawal possibilities.

Anyone who exercises a gainful activity in Switzerland and pays contributions to the AVS can contribute to pillar 3a. This includes:

Pillar 3a allows :

Yes, but at a reduced rate of 1/5 of the tax rate, separate from other income.

You must make Pillar 3a payments no later than December 31 to be tax deductible in the current year.

Yes. In the event of your death, your 3a credit balance is transferred first to surviving spouse or registered partner, then to the children. Failing that, other relatives may be beneficiaries, depending on the law and your beneficiary clause.

Visit 2026the maximum amount is CHF 7,258 per year for employees affiliated to the 2nd pillar. Self-employed people without a 2nd pillar can contribute up to 20 % of their income, with a ceiling of CHF 36,288 per year.

Yes. 3a assets are strictly regulated. Placed with approved insurance companies or banks, they benefit from legal protection and are considered highly secure savings for retirement.

You can transfer the entire balance of your pillar 3a account to another (for example, from a bank to an insurance company) without tax consequences. The transfer amount is unlimited, but fees vary from one provider to another.

There is no “meilleur” pilier 3a universel. Un compte bancaire 3a sera plus flexible et peu coûteux, alors qu’une assurance 3a combine épargne et protection (décès, invalidité). Le choix dépend de votre âge, de votre situation familiale et de votre tolérance au risque.

Make a free appointment with one of our pension experts for personalized advice.