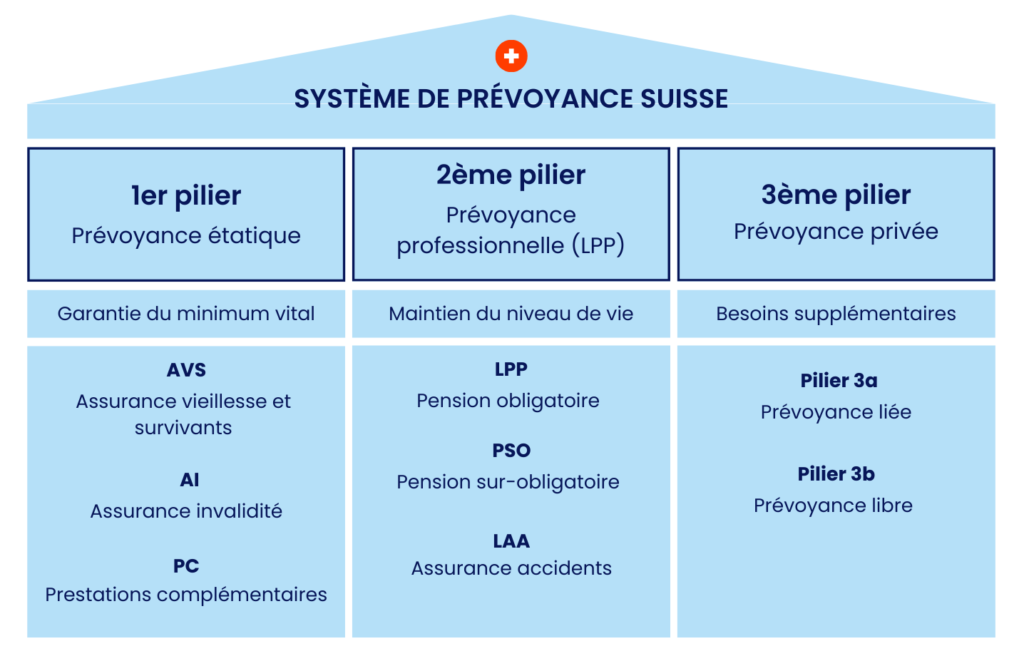

1st pillar: AHV/IV/EL

The 1st pillar: is the foundation of the Swiss social security system. Its main objective is to ensure living wage for the elderly, survivors and the disabled. The aim is not to maintain the usual standard of living, but to avoid economic insecurity.

AHV (Old-Age and Survivors' Insurance)

The AHV is intended for anyone who has reached the legal retirement age or the survivors of a deceased person (spouse, children) in Switzerland.

It is paid in the form of a monthly pension, calculated based on the insured income and the total contribution period (scale 44).

All residents and workers in Switzerland are obliged to contribute to the 1st pillar from the age of 18 (for employees) or 21 (for those not in gainful employment). Contributions are compulsory until the legal retirement age.

IV (Disability Insurance)

IV (or disability insurance) is intended for people who, due to disability, can no longer work fully or partially.The 3-pillar system in Switzerland

DI provides a disability pension, vocational reintegration assistance and rehabilitation measures.

PC (Supplementary benefits)

AHV or IV recipients whose pensions are insufficient to cover vital needs can receive supplementary benefits, which can be defined as financial support to supplement income and cover expenses such as housing or healthcare.

The 2nd pillar: occupational benefits or BVG

The 2nd pillar of the Swiss pension system is a mandatory insurance for employees and optional for self-employed individuals. Its purpose is to supplement the benefits of the 1st pillar in order to maintain one’s standard of living after retirement, in the event of disability, or for the survivors of a deceased insured person.

Purpose and operation

The purpose of the 2nd pillar is to enable policyholders to keep about 60 % of their previous income in retirement, when combined with 1st pillar benefits. It is based on a capitalization system: each insured saves for himself, and the contributions, together with the returns generated by the funds, constitute a capital of individual benefits.

The benefits of the 2nd pillar are therefore not financed on a solidarity basis as in the 1st pillar, but are directly linked to the savings accumulated by the insured person.

Who is concerned by the 2nd pillar?

Affiliation to the 2nd pillar is mandatory for employees whose annual income exceeds a minimum threshold, set at CHF 22,680 in 2024. Self-employed workers are not required to join but may do so on a voluntary basis. For those earning below the minimum threshold, there are non-mandatory occupational pension arrangements available.

Contributions and financing

The financing of the 2nd pillar is based on shared contributions between the employer and the employee. The employer’s share must be at least equal to that of the employee, although many companies contribute more to provide better benefits. The contribution rate increases with the insured person’s age, allowing savings to intensify as retirement approaches.

Contributions consist of two parts:

- Old-age savings : a portion of each contribution is paid directly into the policyholder's individual account.

- Disability and death risks: a fraction of contributions is used to finance disability benefits or survivors' pensions in the event of death.

2nd pillar benefits

2nd pillar benefits take several forms:

- Old-age pension : When you reach retirement age, you can choose to receive a monthly pension or a lump-sum withdrawal. The annuity is calculated on the basis of the capital saved and a conversion rate set by law.

- Disability pension : In the event of disability, the insured receives a pension to compensate for loss of income. It is financed by the portion of contributions earmarked for risks.

- Survivors' pension : In the event of the insured's death, the designated beneficiaries (often the spouse or children) can receive an annuity or a lump sum.

3rd pillar: unrestricted and restricted pension plans (3b and 3a)

The 3rd pillar is the component optional of the Swiss pension system, designed to complete 1st and 2nd pillar benefits. It is based on private savings and offers the flexibility to adapt pension provision to individual needs and objectives. It is particularly important for people wishing to fill the gaps or plan a more comfortable financial future.

Objective of the 3rd pillar

The 3rd pillar aims to allow individuals to anticipate personal needs not covered by the first two pillars. It is designed to finance life projects, build retirement savings, or provide a financial safety net in case of hardship.

It is particularly relevant for self-employed people who do not contribute to the BVG and for those who want to improve their quality of life in retirement.

3a: Tied pension plan

The 3a pillar is specifically designed for retirement and governed by strict rules. It offers significant tax advantages, as contributions made to a 3a account are deductible from taxable income, helping reduce your overall tax burden. In 2024, the maximum deductible amount is CHF 7,258 per year for individuals affiliated with a 2nd pillar, and CHF 36,883 for self-employed persons without occupational pension coverage. In addition, the returns generated by the savings are not taxed as long as the funds remain in the account.

However, 3a funds are locked until a minimum age corresponding to the legal retirement age, except under exceptional circumstances such as the purchase of a primary residence, permanent departure from Switzerland, disability, or the start of self-employment.

3b: Free pension plan

The pillar 3b is highly flexible, allowing you to save or invest without contribution limits or withdrawal restrictions. The money can be used at any time, for example, to finance a project, children's education or to deal with unforeseen circumstances.

It includes products such as savings accounts, life insurance policies, or financial investments. The tax advantages are limited, although some cantons offer deductions for life insurance policies. The 3b pillar is ideal for those who want flexible, unrestricted savings or wish to supplement their retirement planning without the constraints of the 3a system.

Download our pension guide

Invexa's booklet "The pension system explained simply" provides a clear, up-to-date overview of the three pillars of the Swiss pension system (OASI, BVG, 3rd pillar). In just a few pages, you'll discover the 2025 amounts, your rights, and concrete ways to optimize your retirement. An essential guide to understanding, planning and securing your financial future.

Frequently asked questions

A pension gap is the difference between the income needed to maintain one's usual standard of living and the benefits paid by the 1st and 2nd pillars in Switzerland, especially during retirement, in case of disability, or death.

A pension gap can be filled through 3rd pillar contributions, 2nd pillar purchases, life insurance or personal investments.

Swiss pension provision is a social security system designed to guarantee an income in the event of retirement, disability or death. It is based on the three-pillar system:

- State pension scheme (1st pillar),

- Occupational benefits (2nd pillar),

- Individual pension provision (3rd pillar).

- 1st pillar: Anyone living or working in Switzerland.

- 2nd pillar: Employees earning more than CHF 22,680 a year. The self-employed can join voluntarily.

Pillar assets can be withdrawn :

- 1st pillar: Under certain conditions, annuities can be exported, depending on bilateral agreements.

- 2nd pillar: The capital can be withdrawn, except if you remain in the EU/EFTA, where it will be blocked for the compulsory part.

- 3rd pillar A: Funds can be withdrawn in full.