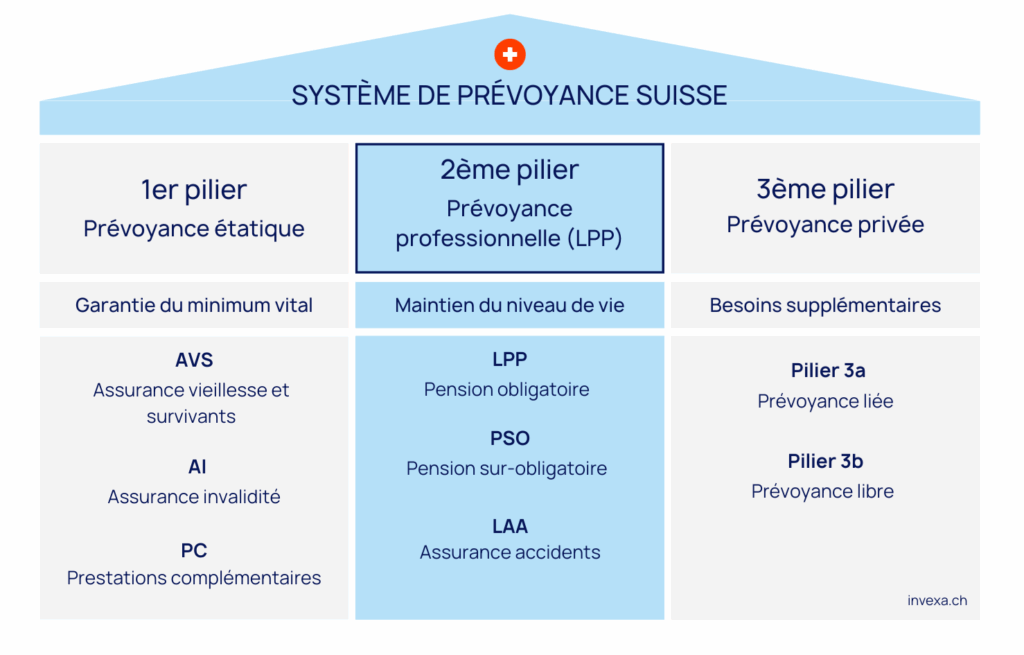

The 2nd pillar (BVG) in brief

- Mandatory at 17 years old (risks) and 25 years old (old age) for employees earning more than CHF 22,680/year

- Employer and employee shared contributions: The employer pays at least 50%

- Conversion rate: 6.8% of accumulated retirement savings

- Withdrawal possible in the form of an annuity, lump sum, or combination: irrevocable decision

- Early withdrawal allowed in 4 cases: Early retirement, real estate purchase, independence, permanent move from Switzerland

- Voluntary buybacks possible and tax-deductible

What is the 2nd pillar?

The 2nd pillar, also known as occupational pension or LPP (Law on Occupational Pensions), is a mandatory insurance system in Switzerland for employees whose income exceeds a certain threshold. It is part of the three-pillar system. Its purpose is to supplement the benefits of the AVS, ensuring a sufficient income in retirement, or in case of disability or death. Funded jointly by the employer and the employee, it is based on the principle of individual capital accumulation: each insured person saves for their own retirement.

Who is concerned?

Not all employees in Switzerland are automatically enrolled in the 2nd pillar. Mandatory affiliation depends on several conditions:

- Be employed and subject to AHV contributions

- Annual income over CHF 22,680 (threshold 2026)

- Must be at least 17 years old for death and disability insurance

- From the age of 24, start contributing to retirement too

LPP Thresholds (2026)

| LPP Setting | Amount |

|---|---|

| LPP entry threshold (minimum income) | CHF 22,680 |

| Coordination deduction | CHF 26,460 |

| Guaranteed minimum coordinated salary | CHF 3,780 |

| Maximum guaranteed coordinated salary | CHF 64,260 |

| Maximum Pensionable Salary | CHF 90,720 |

Even if you do not meet the standard conditions, it is possible to join the 2nd pillar on a voluntary basis. For example, an employer may choose to cover an employee whose income is below CHF 22,680. Likewise, self-employed individuals or those on short-term contracts can opt to contribute, although it is not mandatory. From age 24, contributions also start to build up savings for retirement.

Retirement contributions and bonuses

Contributions to the 2nd pillar (LPP) are calculated on the annual salary says coordinated (i.e. after deduction of a fixed amount known as the coordination deduction, CHF 26,460 in 2026). Contributions are shared between employer and employee, with the employer paying at least half (except for the self-employed, who must pay the full amount). Contributions comprise several components, including retirement savings, risks and expenses.

1. Old-age contribution

Retirement credits represent the savings portion of the occupational pension plan, and the interest rate on these credits is set by the employer. increases with age to gradually build up retirement savings. Here is an overview of retirement credits in 2026, depending on the age of the insured in the compulsory portion:

| Insured's age | Percentage % |

|---|---|

| 25 - 34 years old | 7% |

| 35 - 44 years old | 10% |

| 45 - 54 years old | 15% |

| 55 - 65 years old | 18% |

2. Risk premiums

Risk premiums finance the coverage against the risks of disability and death. This means that if an insured person becomes disabled or dies before reaching retirement age, the pension fund will pay a disability pension or a survivor’s pension (to the spouse, registered partner, or children). These premiums vary depending on age and gender.

3. Contribution to the LPP Guarantee Fund

Each pension institution must pay a contribution to the LPP Guarantee Fund, which secures the statutory minimum benefits in the event of a pension fund’s insolvency. This mechanism protects insured persons from losing their retirement savings if their fund goes bankrupt. The fund also intervenes in cases of restructuring or exceptional situations, such as fund mergers.

Benefits: Old Age, Disability, Death

The 2nd pillar also protects insured persons and their families against the risks of disability or death, as well as the inevitable risk of old age. Benefits are therefore paid out based on different life events, in the form of pensions. Here is a brief overview of the main benefits provided under the LPP:

| Type of pension | Details |

|---|---|

| Retirement | |

| Retirement pension | Paid starting at the legal retirement age. Calculated based on the accumulated retirement savings, at a conversion rate of 6.8%. |

| Retirement capital | You may withdraw one-quarter of your mandatory LPP balance as a lump sum. Some pension funds allow you to withdraw the entire balance. |

| Child benefit for retirees | 20% of the old-age pension paid per child, until the child turns 18 or 25 if the child is in school. |

| Disability before retirement | |

| Disability pension | If the insured person becomes disabled (as defined by the AI), they receive a pension calculated based on their accumulated balance plus future age-related adjustments, without interest. |

| Child disability allowance | 20% of the disability pension paid per child, until the child turns 18 or 25 if the child is in school. |

| Death before retirement | |

| Spouse's pension | The surviving spouse receives 60% of the pension if the marriage lasted at least 5 years and the spouse is at least 45 years old, or if there are dependent children. Otherwise, a lump-sum payment equivalent to 3 annual pensions may be paid. |

| Orphan's pension | 20% of the pension paid to each child until age 18, or age 25 if the child is in school. |

Annuity or lump sum: what to choose at retirement?

Upon retirement, you can receive your vested LPP (Occupational Pension Plan) benefits in the form of a lifelong annuity, a lump sum payment, or a combination of both. This choice is irrevocable and must be communicated to your pension fund at least one year in advance.

The Annuity guarantees a fixed monthly income for life, regardless of your lifespan or market fluctuations. With the statutory conversion rate of 6.8 % on the mandatory portion, it offers a guaranteed return that is difficult to match with safe investments. On the other hand, any remaining capital is not passed on to heirs, and the annuity is taxed at 100 % as income.

The capital It offers complete flexibility—paying off a mortgage, investing, planning an estate—and is taxed only once at a reduced rate upon withdrawal. However, you are solely responsible for managing the capital over 20 to 30 years, with no safety net if the funds run out.

The combination of the two is often the most balanced solution: a portion in annuity to secure a basic income, and a portion in capital for projects and inheritance.

For a numerical analysis, consult our LPP annuity or lump sum.

How can I improve my 2nd pillar benefits?

Performing buying into your pension fund is the most effective way toimprove your services from the 2nd pillar. These payments volunteers allow you to make up any contribution gaps, for example after a change of job, unpaid leave or a reduction in your working hours.

The amount purchased directly increases your retirement assets, which means a higher pension when you retire. In addition to this advantage, purchases are tax-deductible, which means you can reduce your taxable income. However, certain conditions must be met, including a three-year waiting period before a lump-sum withdrawal can be made if you have made a purchase.

To acquire optimize your pensionthe 3rd pillar offers a tailor-made solution that complements your pension fund. Visit Pillar 3a, and the pillar 3b in some cantons, benefit from a recognized tax advantage.

How do I withdraw my 2nd pillar?

The capital in your 2nd pillar can be withdrawn as follows certain conditions:

1. Retirement

You can request payment of all or part of your retirement capital in the form of a lump sum, in accordance with the rules of your pension fund. A formal request must be made several months in advance.

2. Permanent departure from Switzerland

If you leave Switzerland for a country outside the EU/EFTA, you can withdraw your entire 2nd pillar. If you are moving to an EU/EFTA country, only the amount in excess of your compulsory pension can be withdrawn, with some exceptions.

If you have already withdrawn your 2nd pillar upon leaving the country and are considering returning to Switzerland, the consequences for your retirement benefits are significant — find out more. Steps and available options.

3. Access to property

You can use your credit balance to finance the purchase of your principal residence, either by early withdrawal or as a guarantee (EPL - encouragement to home ownership).

4. Start of self-employed activity

5. Small amount

If your vested benefit credit is less than one year's contributions, you can apply to withdraw it.

Taxation of withdrawals

Each withdrawal is subject to the’capital gains tax, a tax on reduced rateseparate from ordinary income, to 1/5 tax rate. It is therefore advisable to plan this operation carefully.

Taxation of Withdrawals

In Switzerland, the withdrawal of LPP capital is subject to a capital gains tax, it is a tax distinct from ordinary income, applied at a reduced rate corresponding to approximately 1/5 of the usual rate depending on the cantons.

The rate varies significantly depending on the canton of residence at the time of withdrawal. For a withdrawal of CHF 200,000, the differences are significant:

| Canton | Estimated rate | Estimated tax |

|---|---|---|

| Zug | ~4,2% | CHF 8,400 |

| Valais | ~5,5% | CHF 11,000 |

| Zurich | ~5,6% | ~CHF 11,200 |

| Geneva | ~5,7% | CHF 11,400 |

| Fribourg | ~5,8% | CHF 11,600 |

| Vaud | ~6,4% | SF 12,800 |

The tax is progressive: The larger the amount withdrawn in a single instance, the higher the effective rate. Splitting withdrawals over several tax years can generate significant savings. For example, in Geneva, two withdrawals of CHF 250,000 spaced one year apart cost approximately CHF 10,500 less than a single withdrawal of CHF 500,000.

Three essential rules to remember:

- Never withdraw capital within 3 years of an LPP withdrawal, or face tax recall.

- Avoid accumulating the LPP withdrawal and the 3rd pillar withdrawal in the same tax year

- For couples, coordinating withdrawals over two distinct years

Special case of French cross-border workers: Withdrawals from the 2nd pillar are subject to several cumulative taxes: Swiss withholding tax, French taxation (a flat-rate levy of 7.5% after a deduction of 10%, or a progressive tax scale), and social security contributions (~9%). On a principal amount of CHF 200,000, the total tax burden can reach CHF 30,000 to 35,000, depending on the situation. Advance planning is essential.

For an accurate estimate of your taxes and an optimized withdrawal strategy based on your canton and family situation, consult our comprehensive guide on Swiss Pension Fund Withdrawal Taxation.

LPP Buyback: Optimize your retirement

Performing buying into your pension fund is the most effective way toimprove your services from the 2nd pillar. These payments volunteers allow you to make up any contribution gaps, for example after a change of job, unpaid leave or a reduction in your working hours.

The amount purchased directly increases your retirement assets, which means a higher pension when you retire. In addition to this advantage, purchases are tax-deductible, which means you can reduce your taxable income. However, certain conditions must be met, including a three-year waiting period before a lump-sum withdrawal can be made if you have made a purchase.

To acquire optimize your pensionthe 3rd pillar offers a tailor-made solution that complements your pension fund. Visit Pillar 3a, and the pillar 3b in some cantons, benefit from a recognized tax advantage.

Dividing the 2nd pillar in the event of divorce

In the event of divorce in Switzerland, the 2nd pillar assets accumulated during the marriage are in principle shared equally between the spouses, regardless of the division of assets or matrimonial property regime. This division concerns only the termination benefits (vested benefits) accrued during the couple's life together.

The amount is calculated as of the date on which the divorce proceedings are initiated. Each spouse is entitled to half pension assets saved by the other during the marriage. If one of the spouses has made little or no contributions (e.g., in the event of a career break to raise children), he or she can recover part of the other's assets in the form of a compensatory allowance.

The amount transferred is paid either into the beneficiary's pension fund or into a vested benefits accountif he is not immediately affiliated to a fund. There are exceptions (e.g. in the case of a different agreement validated by a judge, or where the pension is already in payment), but the principle of sharing remains the rule under Swiss law.

Freedom of movement and change of employment

A Liberty deposit account used for conserve your second pillar assets when leaving a pension fund without immediately joining another. It is a mandatory transitional solution to avoid losing your occupational benefits.

This situation arises in particular if you:

- Leave your job without taking a new one immediately

- Become self-employed

- Reduce your work rate below the LPP threshold

- Are unemployed for a period

- Move abroad

Having accumulated it, it remains blocked, protected, and continues to generate interest, while being exempt from wealth tax. You can transfer it to either a Bank account of free passage, either in a Insurance policy free passage. You thus maintain your link with the provident fund, pending a new affiliation or another event (retirement, repurchase, or early withdrawal under certain conditions). In all cases, compare free passage solutions is essential before making a decision.

Frequently asked questions

The 2nd pillar supplements the AHV and helps maintain approximately 60% income prior to retirement. It is financed by contributions shared between employee and employer.

The second pillar was introduced in Switzerland in 1985 with the entry into force of the LPP.

The average LPP old-age pension in Switzerland amounts to approximately CHF 100,000-150,000, but varies greatly depending on age, salary, and contribution period.

To the retirementor earlier in some cases: definitive departure from Switzerland, purchase of a home, start of self-employment or amount too low.

Every year, your pension fund sends you an annual pension certificate indicating your pension assets and expected benefits.

All 17 years old or more whose annual income exceeds CHF 22,680 (in 2025). The self-employed can join voluntarily.

You can unlock your 2nd pillar in Switzerland when you retire or earlier to buy a home, become self-employed or leave the country permanently.