Why should cross-border commuters think about additional savings?

Income from 1st and 2nd pillars are not enough to maintain a standard of living after retirement, especially for those who have not worked exclusively in Switzerland. The 3rd pillar represents an essential compensation tool. In addition, it offers the possibility of investing in a variety of vehicles, some of which guarantee capital security.

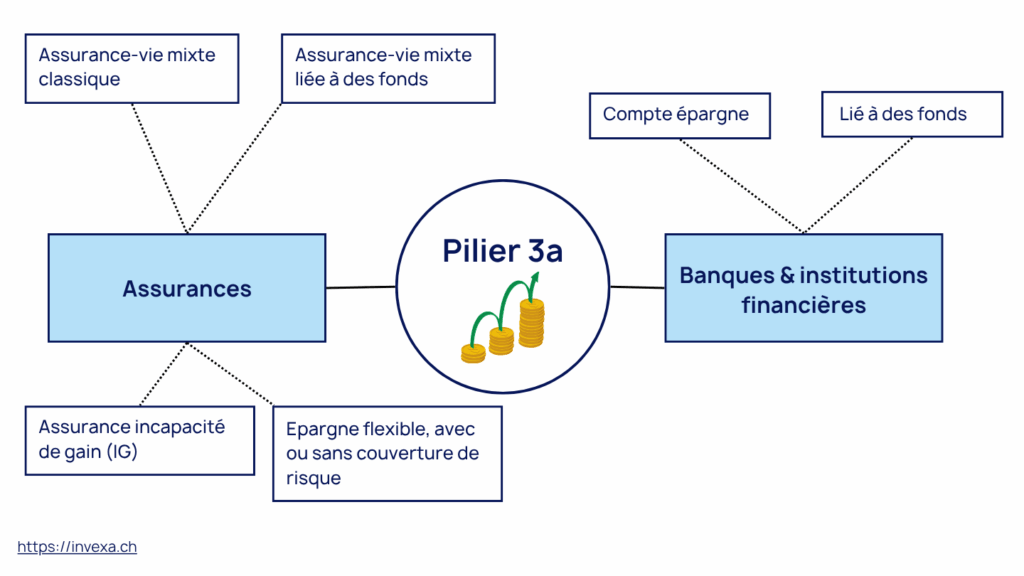

Types of 3rd pillar in Switzerland

In Switzerland, there are two types of third-pillar pensions: the tied personal pension (3rd pillar A)and the unrestricted individual pension plan (3rd pillar B).

Pillar 3A (restricted pension plan)

The Pillar 3a is designed specifically for retirement. The funds paid into it can only be recovered at the time of retirement or under certain conditions. exceptional situations (purchase of principal residence, permanent departure from Switzerland, etc.).

Payments are deductible of taxable income, subject to compliance with certain conditions, in particular for cross-border commuters (for example, the choice of cross-border commuter status). quasi-resident in some cases).

Pillar 3a contribution limits

In 2026, it will be possible to pay out the following amounts in tied personal pension plans:

- Employees affiliated to a pension fund: Up to CHF 7,258 / year

- Self-employed or employees not affiliated to a pension fund: 20% of income, maximum CHF 36,288

The 3rd Pillar A is divided into two categories: in banking and insurance. In insurance, we find classic life insurance (pure risk) or mixed (part of savings in funds or interest-bearing account), but also disability insurance, essential for the self-employed. Increasingly, insurance companies are also offering life insurance contracts. more flexible tied pension planssimilar to the 3a banks, but which offer covers (e.g. waiver of premiums in the event of disability, profit sharing, guarantees, etc.).

3a banking offers a more simple and flexibleThis type of account allows you to pay in the amount you want each year. Essentially, there are two possible forms: the interest-bearing account, linked to a investment funds. No additional coverage is available.

Pillar 3B (unrestricted pension plan)

Unlike the 3A, the 3B is not designed exclusively for retirement. It offers great freedom in the use of funds, which can be mobilized for a variety of projects or financial needs. When we talk about 3B, we mean all the instruments that are not included in the 1st, 2nd and 3rd pillar A. These may include life insurance, classic cars, savings accounts, stocks or bonds, real estate, or even a life insurance contract. life annuity.

Contributions are not capped, allowing everyone to adjust their savings according to their financial situation and personal objectives. 3B offers a number of tax advantages, includingtax exemption on lump-sum benefits on withdrawal (if the pension provision is fulfilled), as well as income tax of only 4% for single-premium life annuities.

Conditions for taking out a 3rd pillar

For cross-border commuters, access to the 3rd pillar, particularly the linked version (3A), is subject to a number of conditions:

- Income subject to AHV: The 3A is intended for people who pay AVS contributions. For cross-border commuters, this means that their working income in Switzerland must be subject to these contributions.

- Tax status and quasi-resident: To benefit from the tax advantages of 3A, a cross-border commuter must opt for quasi-resident status. In practical terms, this means that 90 % of the tax household's income must be taxed in Switzerland. If a significant proportion of income (over 10 %) is taxed in the country of residence (as in France, for example), the quasi-resident option is no longer available.

To sum up, before taking out a 3rd pillar A, it is essential to check that your income from work in Switzerland is subject to contributions. AVSthat it meets the criteria for the quasi-residentin order to benefit from tax benefits. Moreover, quasi-resident status exists only in the cantons of Geneva and Fribourg.

On the other hand, a 3rd pillar B is open to all and offers a complementary savings solution without the constraints of tax status or payment ceilings, giving you the freedom to manage your portfolio for the future.

Depuis janvier 2021, les frontaliers ne peuvent plus demander une rectification de l’imposition à la source via une taxation ordinaire ultérieure (TOU), ce qui annule la déduction fiscale sur leurs versements. Cependant, en obtenant le statut de quasi-resident - conditional on 90 % of household income being taxed in Switzerland - it is possible to reduce taxable income by up to approx. CHF 7,258 per year per person.

Devrais-je souscrire un pilier 3a en tant que frontalier ?

Le pilier 3a est avant tout un outil d’optimisation fiscale. Il permet de déduire les montants versés de votre revenu imposable en Suisse, ce qui en fait un levier particulièrement intéressant pour les personnes soumises aux statut de quasi-résident (Genève et Fribourg).

Pour les frontaliers exerçant dans les cantons de Vaud, Neuchâtel ou du Jura, la situation est différente en raison des accords fiscaux bilatéraux entre la Suisse et la France. Dans ces cantons, les frontaliers sont imposés en France, et non en Suisse. Ils ne paient donc pas d’impôt à la source en Suisse.

Dans ce contexte, souscrire un pilier 3a perd tout son intérêt fiscal.

Faut-il pour autant exclure le pilier 3a ?

- Constitution d’une épargne à long terme

- Cadre sécurisé et discipliné pour préparer la retraite

- Rendements intéressants selon le support choisi

Quelle stratégie 3ème pilier selon votre canton ?

- Canton de travail

- Taxation

- Intérêt fiscal du 3a

- Stratégie conseillée

- Genève / Fribourg

- Autres cantons

No (pas de déduction)

How can I take out a 3rd pillar as a cross-border commuter?

To open a 3rd pillar A as a cross-border commuter, you must be able to provide your G permit. medical questionnaire will be requested at the time of underwriting. Some insurance companies do not ask for a medical questionnaire if the insured is sufficiently fit. young. It is therefore advisable to open a 3rd pillar A account at an early stage.

Optimisez votre 3ème pilier

What 3rd pillar options are available for cross-border commuters?

In Switzerland, very few insurance companies accept cross-border commuters in the 3a category. Pillar 3a bank plans are, however, accessible to cross-border commuters in most cases.

Déclaration annuelle : vos obligations en France

- Le formulaire : Cochez la case 8UU de votre déclaration de revenus (2042) et remplissez l'annexe 3916 (Comptes ouverts à l'étranger).

- Ce qu'il faut déclarer : Le nom de l'organisme (ex: UBS, VIAC, Swiss Life) et le numéro de compte. Les intérêts annuels d'un 3a ne sont pas imposables en France tant qu'ils restent dans le "tunnel" de prévoyance.

- L'amende : L'oubli de cette déclaration peut entraîner une amende de 1 500 € par compte, même si aucun impôt n'est dû.

Retrait du 3ème pilier frontalier : Comment éviter la double imposition ?

C’est la crainte numéro un des travailleurs frontaliers : vais-je être imposé deux fois au moment de retirer mon 3ème pilier ? Une fois par la Suisse, et une fois par la France ?

La réponse courte est : no. La convention fiscale franco-suisse est justement conçue pour empêcher cette double imposition. Cependant, le mécanisme prend la forme d’une avance de frais. Si vous ne faites pas les bonnes démarches, vous risquez effectivement de perdre de l’argent. Voici exactement comment se déroule la fiscalité à la sortie.

Impôt à la source prélevé par la Suisse (avance)

Au moment où vous débloquez votre capital (pour la retraite, l’achat d’une résidence principale ou un départ définitif), la Suisse ne vous verse pas 100 % de la somme.

L’institution de prévoyance (votre banque ou votre assurance) a l’obligation légale de retenir un impôt à la source. Ce n’est pas une pénalité, mais une garantie pour l’État.

Le taux de cet impôt ne dépend pas de votre canton de travail, mais du canton où est domiciliée la fondation de votre 3ème pilier. (C'est pour cela que de nombreuses fondations s'installent dans des cantons à la fiscalité avantageuse, comme Schwyz).

Obligation de déclaration en France

En tant que résident fiscal français, vos revenus mondiaux doivent être déclarés en France. Le retrait de votre 3ème pilier n’y fait pas exception. L’année suivant votre retrait, vous devez déclarer ce capital à l’administration fiscale française (via les formulaires de revenus encaissés à l’étranger, type 2047, et la déclaration classique 2042).

La France appliquera alors sa propre fiscalité sur ce capital (un prélèvement forfaitaire de 6.75 % sur le capital, auquel s’ajoutent les prélèvements sociaux de la CSG/CRDS).

Pour éviter cette fameuse double imposition, la convention bilatérale franco-suisse vous permet de récupérer l’intégralité de l’impôt à la source qui vous a été prélevé par la Suisse lors du retrait.

Vous disposez d'un délai de 3 ans après le versement de votre capital pour réclamer le remboursement de cet impôt à la source suisse. Passé ce délai, les fonds sont définitivement perdus au profit du fisc suisse.

Designing a savings strategy with the 3rd pillar

1. Define your goals

To begin with, it's essential to clearly define your savings objectives. This means identifying whether you simply want to build up savings for the future. retirement or if you also need to cover risks such as theearning incapacitythe deathor other financial contingencies. Once you've established your goals, you'll know whether you need a full coveragea simple funds savings plan or other solution to meet specific short- or medium-term needs.

2. Define your investor profile

Next, it is important to assess your investor profile in order toadapt your strategy to financial market fluctuations. To do this, you need to determine your risk tolerance and your investment horizon. An investor curator profile will prefer low-risk, moderate-return funds or a simple savings account, while a more dynamics could opt for more aggressive investments.

This personal analysis is essential for choosing products that match your needs. preferences and your situation current financial situation.

3. Compare funds and performance

Once your objectives and investor profile have been clearly defined, it's time to compare different offers available. This involvesanalysis performance historical and fees associated with 3rd pillar funds. You can compare the returns of guaranteed funds, unsecured funds and investment funds. actions or even solutions mixedkeeping in mind that the diversification remains an important lever for optimizing returns and limiting risks. A detailed comparative analysis will enable you to select products suited to your savings strategy.

4. Combining contracts

Finally, to maximize the tax benefits of the 3rd pillar, it may be wise to combine several contracts. Subscribing to several products allows you to make staggered withdrawals and therefore reduce your marginal tax ratetaxation.

Frequently asked questions

Yes, cross-border commuters can take out a 3rd Pillar A, even if they live in France. This savings product is open to anyone working in Switzerland.

However, the Swiss tax advantage (deduction of payments from taxable income) is only available to cross-border commuters who have opted for quasi-resident status via T.O.U. (Taxation ordinaire ultérieure), i.e. in Geneva and Fribourg only.

Oui, mais sous condition. Depuis 2021, seuls les frontaliers ayant le statut de quasi-resident (plus de 90 % de leurs revenus mondiaux perçus en Suisse) peuvent déduire leurs cotisations 3a de leur impôt à la source. Cela concerne principalement les travailleurs des cantons de Geneva and Fribourg.

Le montant maximum déductible pour un salarié affilié à une caisse de pension (2ème pilier) est de CHF 7,258 per year. Pour les indépendants sans 2ème pilier, le plafond est de 20 % du revenu net, jusqu’à un maximum de CHF 36,288.

Oui, mais l’avantage ne sera pas fiscal en Suisse car l’impôt est payé en France (selon l’accord de 1983). Le 3ème pilier reste toutefois intéressant pour l’épargne de prévoyance, le rendement des fonds de placement, et les couvertures d’assurance (décès/invalidité) souvent plus protectrices qu’en France.

Vous devez signaler la détention de votre compte ou contrat chaque année via le formulaire 3916 (comptes à l’étranger) et cocher la case 8UU de votre déclaration de revenus 2042. Aucun impôt n’est dû sur les intérêts annuels tant que le capital n’est pas retiré.

Le retrait est possible pour trois motifs principaux : l’âge légal de la retirement, l’achat de votre principal residence (en France ou en Suisse), ou le lancement d’une activité indépendante.

Oui. Le capital retiré est imposé en France, généralement via un prélèvement forfaitaire de 6.75 % (plus prélèvements sociaux). L’impôt à la source prélevé par la Suisse au moment du versement vous sera intégralement remboursé après avoir prouvé votre déclaration au fisc français.

The 3rd pillar supplements the 1st and 2nd pillars (AVS/AI and LPP) to maintain your standard of living in retirement.

- The pillar 3a (linked) is a locked-in savings up to 5 years before retirement, with tax benefits under certain conditions.

- The pillar 3b (free) offers greater flexibility and can be used as savings, life insurance or investment, with no payment limit.

From 2021The classic deductions linked to the 3rd pillar (and other expenses) are only possible for cross-border commuters with quasi-resident status (T.O.U), i.e. when 90 % of household income is taxed in Switzerland.

If you complete this conditionPillar 3a contributions can be deducted from your Swiss taxable income, up to a maximum of CHF 7,258 per year in 2025. Otherwise, you won't benefit from any tax deduction, but you can still save freely in a 3b to prepare for your retirement.

3rd Pillar A funds can be withdrawn in the following ways following cases:

- Definitive departure from Switzerland,

- Transition to self-employment,

- Purchase or repayment of a main property,

- Purchase of 2nd pillar contributions,

- Retirement (up to 5 years before legal retirement age).

Withdrawal is subject tocapital gains taxat a reduced rate. 3rd Pillar B funds, on the other hand, are free to withdraw, subject to the conditions set out in the contract.