In Switzerland, buying a property is generally done through a mortgage loanbank financing based on the pledging of the property. It's an accessible solution, but subject to strict rules. For example, banks require a down payment of at least 20 % of the property's price and assess the borrower's financial viability using the debt ratio and disposable income.

With so many offers available and so many different financing options, it's essential to understand the mechanics of mortgages to avoid the pitfalls and optimize your real estate investment.

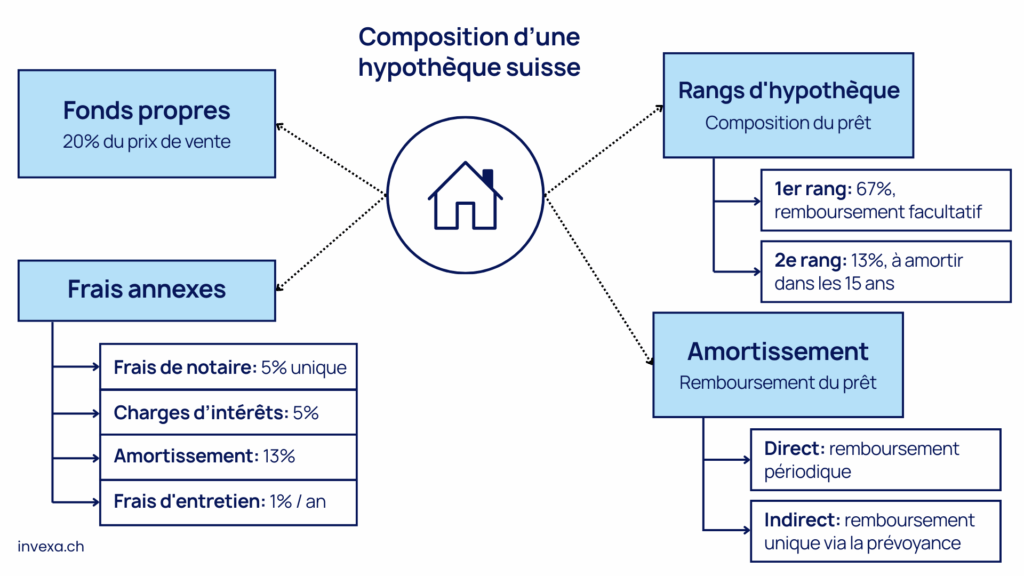

A mortgage is made up of several key elements that define its cost, structure and repayment.

This is the amount that the bank or lending institution makes available to the borrower to finance the purchase of the property. In Switzerland, this amount can cover up to 80 % of the property's value, the 20 remaining % to be financed by the buyer's personal contribution.

Example For a property in CHF 1,000,000mortgage can be up to CHF 800,000with a personal contribution of CHF 200,000.

These are the fees the borrower pays to use the money lent. They vary according to the type of rate chosen.

The mortgage rates are regularly updated and should be compared before making a choice.

Amortization is the gradual repayment of borrowed capital. In Switzerland, there are two types of amortization :

In addition to interest and principal, there are other costs associated with a mortgage:

Underwriting a mortgage in Switzerland follows a structured process, from validation of equity to analysis of financing capacity. Find out more about 7 key steps to understand banking requirements and finance your real estate financing contract.

The most common source of equity is personal savings accumulated in bank accounts or in the form of financial investments, but there are other ways of obtaining equity.

It is possible to use part of its 2nd pillar (LPP pension fund) to finance a property for personal use (principal residence only).

Two options are available: EPL pledging and early withdrawal.

Pledging means offering your 2nd pillar as collateral to the bank without withdrawing the capital. This enables you to obtain a higher mortgage. Your pension capital remains intact in your pension fund, so your benefits will not be affected. What's more, you can pledge all or part of your BVG/LPP credit.

Terms and conditions:

Advantages:

The early withdrawal is to withdraw part of your 2nd pillar before retirement age to finance the purchase of a property to be used as your principal residence.

Terms and conditions:

Advantages:

It's advisable to run scenarios of early retirement and pledging before making a decision. Ultimately, with a pledge, you can keep your benefits and your assets continue to grow, but you will pay higher interest charges. With an EPL withdrawal, interest charges are lower, but pension fund benefits are also reduced, plus income tax on the withdrawal (refunded if the asset is sold).

The 3rd pillar (restricted and unrestricted private pension plans) , whether in the 3a or the 3b, is an interesting solution to complement equity required for a mortgage. As with 2nd pillar:, There are two possibilities: withdrawal or pledging. The conditions are almost identical.

A 3rd pillar insurance is recommended when taking out a mortgage, in particular thanks to the release of premiums or annuity in the event of disability, which will enable the mortgage to be retained in the event of disability.

The indebtedness ratio is defined as the percentage of your annual revenues that goes towards paying off your mortgage. To calculate it, you need :

This ratio enables banks to assess your ability to bear the cost of a loan. reimbursement of the mortgage. In Switzerland, it is recommended not to exceed a debt ratio of approx. 33%. For example, if your annual expenses are CHF 30,000 and your gross annual income is CHF 100,000, your debt ratio will be (30,000 / 100,000) × 100 = 30%.

Use our mortgage calculator and find out exactly what you can afford.

The reference interest ratecalculated since 2008 on the basis of the average bank mortgage rate and rounded up to the nearest quarter of a percent, is used to adjust rents in line with market fluctuations. Currently set at 1.5 % since 04.03.2025This rate reflects changes in financing conditions, and has a direct impact on the cost of mortgages, whether fixed-rate or variable-rate. fixed rate or based on SARON.

At the same time, the policy rate, determined by the Central bank, The key interest rate influences all market rates. A fall in the key interest rate tends to reduce mortgage rates, which in turn can lead to a reduction in the benchmark interest rate and therefore to more moderate rent adjustments. Banks often offer lower rates, which is why it is essential to compare rates in order to negotiate as effectively as possible.

When it comes to financing a property, it's important to choose the interest rate model that best suits your profile and financial expectations. Here's a comparison of the three main options:

Total transparency, generally the the cheapest historically.

The choice between these models will depend primarily on your risk tolerance and your ability to manage uncertainty. If you prefer predictability and stability of your payments, a fixed rate is a reassuring option. If, on the other hand, you're prepared to accept variations to potentially benefit from more advantageous rates, the variable or SARON can be considered. A thorough analysis of your financial situation and economic outlook is essential to make the most appropriate choice.

When putting together your mortgage file, it is essential to present a complete set of documents attesting to your financial situationthe stability of your income and the value of the property you wish to acquire. These supporting documents enable the bank to assess your borrowing capacity and determine financing conditions most suited to your profile (non-exhaustive list).

To demonstrate the solidity of your income, you will need to provide several documents that will allow the bank to verify your financial situation. professional stability and your annual income. This often includes :

Bank statements are also essential to demonstrate your financial management and the availability of your funds. They allow the bank to examine your savings and spending habits. We recommend that you provide :

In Switzerland, you are often required to have a personal contribution of at least 20 % of the purchase price of the property, part of which must be non-borrowed equity. To prove this, you can present :

To compile a complete file on the property, it is essential to gather all the documents and information attesting to its value. value and its status. These documents not only give the buyer a better understanding of the property, but also enable the bank to accurately evaluate the financing. Here are the main items to be provided:

Banks aren't the only players in the mortgage market. Many other financial institutions also offer real estate financing solutions. For example, the pension fundsPension fund managers often offer mortgages on attractive terms to their members. Similarlyinsurance and investment foundations offer mortgage products, each with its own terms and requirements.

The financing conditions can vary considerably from one institution to another. Each institution defines its own criteria in terms of interest rate, repayment period and ancillary charges, which can influence the total cost of credit. That's why it's essential to compare offers from several providers to find the one that best suits your financial situation and objectives. This diversity of options gives you access to tailor-made solutions, adapted to borrower profiles and the specificities of the real estate market.

Once you've selected the offer best suited to your situation, put together a complete file and negotiated the financing terms, the final step is to take out a mortgage. This is the moment when you formalize the agreement with the financial service provider and legally commit to your real estate project.

Before signing, take the time to reread all the clauses of the loan contract carefully, checking in particular:

Each provider can offer different conditions in terms of rates, duration and fees.

The debt ratio is the proportion of your gross annual income devoted to mortgage repayments (interest and amortization). To calculate it, simply divide your total annual expenses by your gross income and multiply the result by 100.

In Switzerland, it is recommended that this rate should not exceed 33 %.

Disclaimer: The information presented in this article is for information purposes only. It does not constitute personalized financial advice. Investment and pension decisions must be assessed on the basis of your personal situation. An individual analysis is essential.