Life Insurance in Switzerland: 2026 Guide & Independent Advice

FINMA-authorized insurance intermediary

Why life insurance?

A death or a loss of earning capacity can disrupt a family’s financial stability. Life insurance helps protect your loved ones by guaranteeing a lump sum or an annuity, in order to maintain their standard of living and cover ongoing financial commitments, such as a mortgage.

With the right coverage, you can ensure the security of your loved ones and the continuity of your projects, even if the unexpected happens.

Every situation is unique: young parents, homeowners, the self-employed or future retirees. We analyze your needs (family protection, estate planning, retirement provision) to build a customized plan that matches your objectives and your budget.

As an independent brokerage, we have access to all Swiss insurance companies. We compare premiums, benefits, and available options to find the most advantageous and transparent life insurance for you.

Your needs change over time: marriage, birth, property purchase or preparation for retirement. We adjust your policy to reflect these stages of your life, and remain on hand to provide you with lasting advice in a relationship based on trust.

How to take out life insurance in Switzerland

Invexa can help you assess your future needs, optimize your assets and define a clear, personalized strategy.

01

Contact Us

Contact us via our contact form or call us at your convenience.

02

We analyze your needs

A dedicated advisor will analyze your file and arrange a meeting with you to suggest suitable products.

03

Receive your offers

Once we've identified your needs, we'll send you several offers that match your objectives.

04

Get insured

Choose the offer that best suits your needs. Our team will be happy to assist you throughout the process.

Types of life insurance in Switzerland

Life insurance in Switzerland comes in a variety of forms, depending on the policyholder's needs: protection against premature death, disability or building up capital for retirement.

| Type of Insurance | Description | Main Variants |

|---|---|---|

| Life insurance | Capital paid to beneficiaries in the event of death during the coverage period. |

|

| Loss of earnings insurance | Annuity paid in case of income loss due to an accident or illness |

|

| Capital insurance | Combine savings and protection. Capital guaranteed at maturity or upon death |

|

| Life annuities | Stable income guaranteed after retirement, for life or a fixed period |

|

Life insurance

Death risk insurance is one of the most common types. It guarantees the payment of a lump sum to the beneficiaries in the event of the insured’s death during the coverage period of the policy.

It can be taken out on a single life, where only one person is covered, or on two lives, where the capital is paid to the survivor in the event of the death of one of the two insured. There are also variants based on the insured amount: level capital, where the amount remains the same throughout the policy, and decreasing capital, where the capital gradually decreases, often in connection with a mortgage.

Disability insurance

The income protection insurance covers the risk of income loss due to an accident or illness. If the insured becomes unable to work, they receive a benefit after a defined waiting period. This benefit is calculated based on the degree of disability and ends when the insured regains the ability to earn or reaches retirement age.

This type of insurance is particularly useful for self-employed individuals, who do not have coverage under the second pillar, as well as for employees who wish to supplement their disability benefits.

Capital insurance

Capital insurance, also known as savings insurance, combines financial protection with a long-term savings strategy. Survival insurance guarantees the payment of a lump sum to the insured if they are alive at the end of the policy term. In the event of death before this term, the beneficiaries receive at least the total premiums saved.

Endowment life insurance, on the other hand, combines savings and protection: if the insured survives, they receive a lump sum, and in the event of death, the beneficiaries receive an amount specified in the policy.

Unit-linked life insurance offers higher return potential than traditional insurance, as the savings are invested in the financial markets. The insured selects the funds they wish to invest in, thereby accepting a higher risk in exchange for greater potential gains. However, unlike traditional policies, the insurer does not guarantee a minimum capital at the end of the policy term.

Life annuities

Finally, retirement annuities or life annuities are designed to provide a stable income after retirement. They can be immediate, when the annuity starts right after subscription following a single premium, or deferred, when the insured contributes over several years before receiving their annuity.

They can be paid for life or for a fixed period, and some allow the remaining capital to be returned to heirs in the event of premature death.

- 4 good reasons to subscribe

Advantages of life insurance in Switzerland

Life insurance offers many advantages and can be adapted to every stage of your life.

Protect your loved ones

In the event of death, it provides a lump-sum payment to loved ones, ensuring their financial security and standard of living.

Benefit from tax advantages

Depending on the life insurance contract, there are numerous tax advantages, such as tax exemption on withdrawal, deduction of 3a payments, and much more.

Build up your savings

Choose a combined policy for death protection and a savings or investment component, offering a dual function: protection for the family and building up capital for future projects.

Plan your succession

Life insurance makes it easier to pass on your estate by allowing you to designate beneficiaries directly, which can avoid inheritance disputes.

What our customers say

Read the testimonials of our customers who have placed their trust in Invexa for their life insurance.

Publié surTrustindex vérifie que la source originale de l'avis est Google. Mme Fivaz est très avenante, répond aux questions possible et donne les meilleures conseils pour votre 3eme pilier! Très satisfait !Publié surTrustindex vérifie que la source originale de l'avis est Google. Je recommande vivement à toute personne souhaitant réaliser une analyse de marché afin de mieux comprendre les produits d’assurance et de prévoyance. L’accompagnement est clair, structuré et permet d’y voir beaucoup plus clair dans un domaine souvent complexe.Publié surTrustindex vérifie que la source originale de l'avis est Google. Très pro et super réactivité !Publié surTrustindex vérifie que la source originale de l'avis est Google. Très bonne expérience. Échanges professionnels, clairs et menés avec beaucoup de sérieux. Claire s’est montrée disponible, attentive et bienveillante, avec des explications transparentes et un suivi rigoureux, sans aucune pression. Merci pour la qualité de l’accompagnement.Publié surTrustindex vérifie que la source originale de l'avis est Google. Bonjour; j'ai été absolument ravie d'obtenir d'Invexa une réponse si rapide et si complète à ma question concernant les allocations pour enfants. Je remercie de tout coeur la conseillère pour son empressement à me répondre. Merci.Publié surTrustindex vérifie que la source originale de l'avis est Google. I received great advice and very friendly service. I wholeheartedly recommend Invexa for anything pension-related. Best regards, Anetta ZargaryanPublié surTrustindex vérifie que la source originale de l'avis est Google. Services très professionnels. Bonne compréhension des enjeux et grande amabilité.Publié surTrustindex vérifie que la source originale de l'avis est Google. De très bon conseil. MerciPublié surTrustindex vérifie que la source originale de l'avis est Google. J'ai fait un entretien avec Mme Fivaz concernant mon 3e pilier. Elle a su répondre à toutes mes questions avec bienveillance et clarté. Je recommande à 100%!Publié surTrustindex vérifie que la source originale de l'avis est Google. Les conseils de Mme Fivaz sont clairs et concis ! J’ai beaucoup apprécié l'échange sympathique et je ne peux que recommander ses services et son conseil attentionné. Merci beaucoupCertifié par: TrustindexLe badge vérifié de Trustindex est le symbole universel de confiance. Seules les meilleures entreprises peuvent obtenir le badge vérifié, avec une note supérieure à 4.5, basée sur les avis des clients au cours des derniers 12 mois. En savoir plus

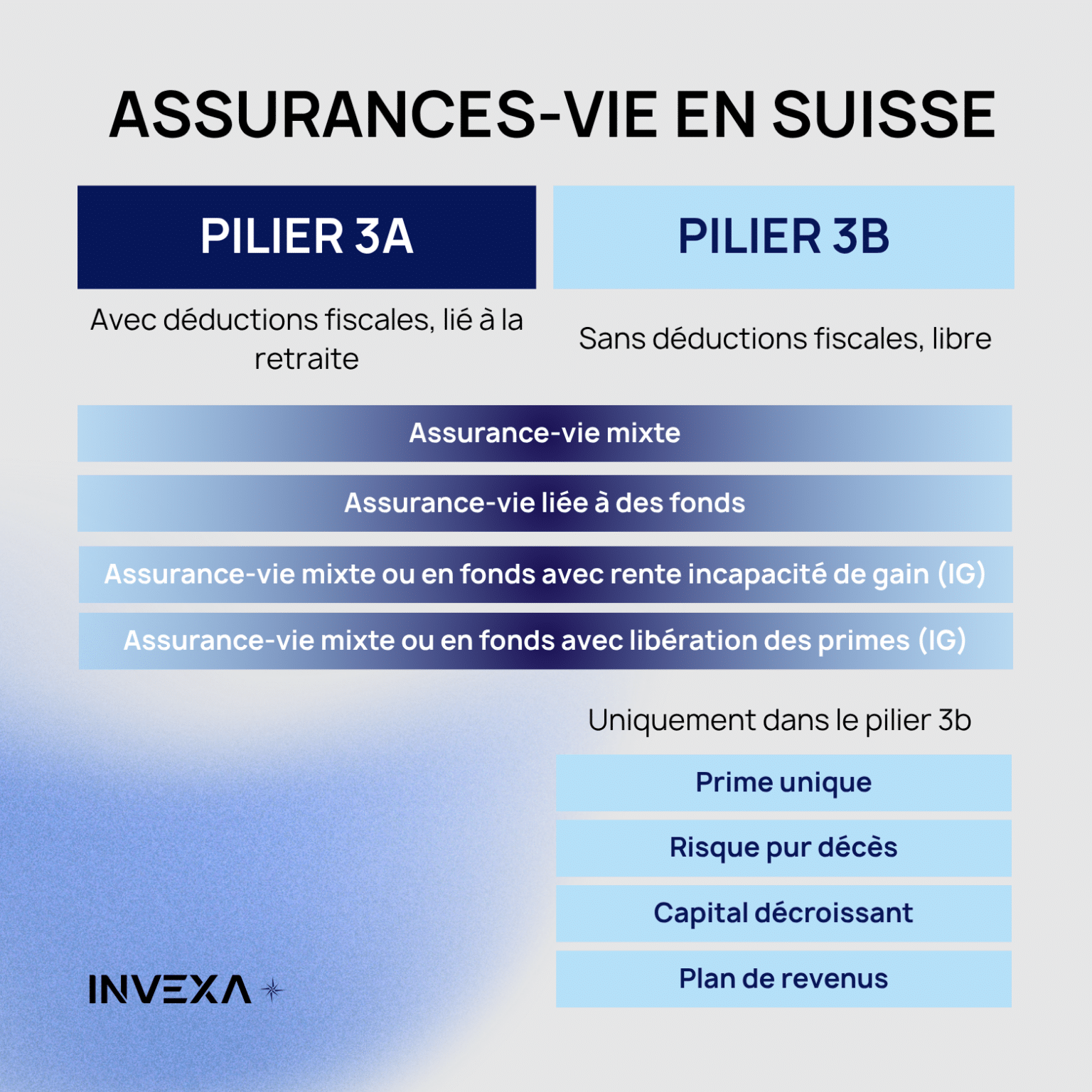

Should you choose Pillar 3a or Pillar 3b in 2026?

This is the most frequently asked question by our clients. In terms of life insurance, the Swiss pension system offers two very different legal vehicles: tied pension (Pillar 3a) and flexible pension (Pillar 3b).

Making the wrong choice here will cost you not only in flexibility; it can also cause you to lose thousands of francs in tax deductions. Here’s the fundamental difference: Pillar 3a optimizes your immediate taxes at the expense of liquidity, while Pillar 3b offers total freedom with a tax advantage specific to residents of Geneva and Fribourg.

Quick comparison: Pillar 3a life insurance vs. Pillar 3b

| Feature | Pillar 3a (Tied) | Pillar 3b (Flexible) |

|---|---|---|

| Main Objective | Pure retirement savings & strong tax optimization | Flexibility, medium-term projects & wealth transfer |

| Tax Deduction | Yes. Deductible from federal and cantonal income (up to the legal maximum) | Not at the federal level. But yes in Geneva (e.g., up to CHF 2,345 for a single person) |

| Capital Availability | Locked. Early withdrawal limited (main home purchase, leaving Switzerland, self-employment) | Free. Withdrawal possible at any time (subject to policy surrender conditions) |

| Beneficiary Clause | Strict. Defined by law (spouse, then children, etc.). Cannot be freely modified | 100% flexible. You choose who receives the capital (partner, friend, foundation), outside of forced heirship rules |

| Taxation at Maturity | Taxed at a reduced rate (separate from other income) | Tax-exempt (if pension conditions are met: contract >5 years, payments after age 60) |

Don’t choose one or the other by default. In over 70% of portfolio optimizations at Invexa, the winning strategy is to combine both. We first max out your Pillar 3a to take full advantage of the federal tax benefit, then use a tailored Pillar 3b life insurance to cover your risks (death/disability) or finance your medium-term projects.

Frequently asked questions about life insurance in Switzerland

Here are the answers to the most frequently asked questions about health insurance in Switzerland.

Protection for Family and Loved Ones: To guarantee a lump sum or annuities to beneficiaries in the event of death, helping maintain their standard of living, repay debts, or finance education.

Retirement Planning: An endowment or unit-linked life insurance can be used to save for retirement while also providing protection in case of death.

Coverage Against Work Disability: Some life insurance policies can be taken out to protect against income loss due to inability to work caused by illness or accident.

Tax Optimization: Certain life insurance policies, such as those linked to Pillar 3a (individual pension plan), offer tax benefits in Switzerland.

A life insurance policy is a contract that allows you to save money and/or benefit from financial protection for yourself and your loved ones in the event of death or disability. It is often used for pension planning, estate planning, and tax optimization.

In Switzerland, life insurance offers tax advantages, especially when taken out within the framework of Pillar 3a (individual pension plan).

Premiums paid are tax-deductible from taxable income up to CHF 7,258 per year for employees and up to 20% of net income (capped at CHF 36,288 per year) for the self-employed. Additionally, the savings capital is not taxed as part of wealth while it remains in the 3a account. The capital is only taxed upon withdrawal, at a reduced rate.

In Geneva and Fribourg, contributions to pillar 3b insurance are deductible from income. The amounts from 2026 onwards are as follows:

- In Geneva: up to CHF 2,345 / year for a single person, 3,518 for a married couple (+959 CHF per child)

- In Fribourg: CHF 750 / year for one person, and CHF 1,500 for a married couple

The term of a life insurance policy is defined from the outset and should be assessed based on risk coverage needs and investment horizon. It can generally range from 5 to 40 years.

In case of termination before the end of the contract, the surrender value may be less than the premiums paid. It is therefore crucial to define the adequate duration from the outset.

- Pure risk life insurance (death): Fixed term (5 to 30 years), ending upon death or at the policy’s maturity.

- Endowment life insurance (savings + protection): Often between 10 and 30 years, sometimes up to retirement.

- Tied Pillar 3a: Up to retirement age (64–65 years), with early withdrawal possible under certain conditions.

- Flexible Pillar 3b: More flexible, typically with a term between 5 and 30 years.

- Investment-linked life insurance: Generally 10 to 30 years, but depends on the investment.

- Whole life insurance: For life, with annuity payments continuing until death.

The cash surrender value of a life insurance policy is the amount the insured can recover if they decide to terminate their policy before its maturity. It mainly applies to life insurance policies with a savings component, such as endowment or investment-linked life insurance.

When taking out a life insurance policy, the policyholder must choose a premium payment method. There are two main options: periodic premiums and a single premium.

The annual premium is a payment method where the insured pays their premium annually/half-yearly/quarterly/monthly, according to the amount specified in the policy. A single premium corresponds to a payment made all at once at the start of the policy. The insured thus covers the entire cost of their life insurance upon subscription.

Yes, life insurance policies must be declared to the tax authorities. Taxation varies according to :

- Premiums paid,

- Cash surrender value (3b only),

- Annuities received, etc. Gains often benefit from advantageous tax treatment, but it is advisable to consult a tax advisor to ensure that all reporting obligations are met.

Funds can be released in several situations:

- Contract expiry date : You receive the lump-sum or annuity payments.

- Partial or total repurchase : You can request early surrender of the contract, which involves recovering the surrender value, possibly subject to fees or penalties.

- Special cases : Certain exceptional events (disability, proven financial difficulties, etc.) provide for specific unlocking procedures.

Life insurers guarantee benefits and fixed premiums over a long period (20 to 30 years). To ensure this stability, they apply a safety margin by overestimating costs and underestimating returns. When management results are more favorable than expected, surpluses are generated:

- Risk premiums : Fewer claims than forecast.

- Savings bonuses : Better investment performance.

- Expense premiums Actual costs lower than estimated.

Surplus earnings can be redistributed to the customer, but this participation is not guaranteed and depends on the insurer's financial results. Once paid out, surpluses belong to the customer and cannot be taken back.

Our skills at your service

We provide comprehensive support to secure your financial future and optimize your assets. Whether you want to finance real estate, plan for retirement, analyze your pension, or recover forgotten occupational pension (LPP) assets, our experts guide you every step of the way.

Retirement Planning

Preparing for retirement means anticipating future income and needs. We draw up a personalized 3-pillar plan to guarantee a worry-free retirement.

BVG asset management

We'll find your forgotten BVG assets and help you consolidate them into a suitable solution to secure your acquired rights.

Insurance brokerage

We compare Swiss insurance companies to offer you clear, tailor-made cover for both your private and business needs.

Mortgage

We can help you find the most suitable mortgage by comparing rates and conditions with the main players on the market.

Pension Analysis

We analyze your benefits and assets to identify gaps and propose solutions tailored to your future needs.

Pillar 3a solutions

We analyze your benefits and assets to identify gaps and propose solutions tailored to your future needs.

Pillar 3b solutions

We'll help you choose a flexible 3b solution to protect your family or save as you wish.

Get personalized advice

Make a free appointment with one of our pension experts for personalized advice.

Claire Fivaz

Request a quote for your life insurance

Fill out this form to schedule a life insurance consultation in Switzerland. Our experts will contact you within 24 hours.