What is a 2nd pillar purchase?

A buy-in to the 2nd pillar involves voluntarily paying a sum into your pension fund to fill gaps in your retirement coverage. These gaps may be due to periods without affiliation (studies, time abroad, career breaks) or a change to a pension plan offering higher benefits.

Each pension institution sets the maximum buy-in amounts according to its regulations and your personal situation: age, insured salary, contribution period, and accrued benefits.

Why buy back my 2nd pillar?

1. Improving performance

The first advantage of a purchase is the increase in retirement capital. This capital will influence..:

- The BVG pension amount that you will receive upon retirement;

- Or the capital that you can withdrawif you opt for a lump-sum payment or in the case of an EPL.

The earlier you make a buy-in during your working life, the more the amounts contributed will benefit from interest and capitalization offered by the pension fund. This can result in a higher pension of several hundred francs per month at retirement.

2. Tax benefits

Amounts paid as part of a buy-in are fully deductible from taxable income at the federal, cantonal, and municipal levels (Art. 33 LIFD).

3. Flexibility in tax planning

Unlike compulsory contributions, buy-backs are optional and modular:

- You can distribute over several years to optimize tax savings;

- You can choose the most opportune time (bonus year, property resale, or drop in income, for example).

Tax advantages of buying into your pension fund

Buying into the 2nd pillar offers exceptional tax advantages, making it the preferred tax optimization tool for middle- and high-income Swiss taxpayers.

Full, unlimited tax deduction

Amounts paid as part of a buy-in are fully deductible from taxable income at the federal, cantonal, and municipal levels (Art. 33 LIFD).

This deduction applies on’year of payment and appears directly on your tax return.

Major advantage over 3rd pillar While the Pillar 3a caps the deduction CHF 7,258 for salaried employees (2026), there is no annual limit on 2nd pillar purchases. Your redemption ceiling depends solely on your pension gaps, These can be as much as CHF 50,000, CHF 100,000 or even more, depending on your situation.

This fundamental difference makes the LPP buy-in the most effective tax-saving instrument for taxpayers who have already maxed out their 3rd pillar.

Calculating real tax savings

The tax savings generated by a buyback depend on three main factors:

1. Your marginal tax rate: The higher your income, the more you are taxed in the higher brackets. If you buy back your income, you'll be taxed in the lower brackets, maximizing your savings.

2. Your canton of residence: Tax rates vary considerably between cantons. Geneva and Vaud apply higher rates than Valais or the canton of Zug, which increases potential tax savings.

3. Your family situation: Married couples, single-parent families and singles benefit from different rates.

In practice, the tax saving generally represents 25% to 45% of the amount bought back.

A concrete example of tax savings

- Profile: Single, 42 years old, no children

- Canton: Vaud

- Taxable income: CHF 120,000

- Purchase amount: CHF 30,000

- Without buyback

- With buyback

- Taxable income

- Total taxes (federal + cantonal + municipal)

- Tax savings

-

This example is indicative and may vary according to social deductions, professional expenses and commune of residence.

Optimization strategies

Spread redemptions over several years

- Remain in more favorable tax brackets

- Maximizing the total tax deduction

- Smooth out the impact on your cash flow

Spread redemptions over several years

- Year of bonuses or exceptional income: A buyback allows you to compensate for a one-off increase in income and avoid falling into a higher bracket.

- Year of taxed capital gains: Ideal for partially neutralizing the taxation of a property sale

- Before a change of canton: If you're moving to a lower-tax canton, make your buy-backs before you leave to maximize the deduction.

Coordination with Pillar 3a

The optimal strategy generally consists of:

- First pour the maximum into the pillar 3a (CHF 7,258 in 2026)

- Then perform 2nd pillar purchases with remaining funds available

This approach makes it possible to combine the benefits of both pillars while maximizing the overall tax deduction.

From 2026 (for fiscal year 2025), it will also be possible to make Pillar 3a purchases.

Beware of tax traps

If you are considering an early withdrawal (property purchase, leaving Switzerland, becoming self-employed), avoid any buy-in during the previous 3 years. The tax authorities would retroactively cancel the deduction, forcing you to repay the tax savings along with default interest.

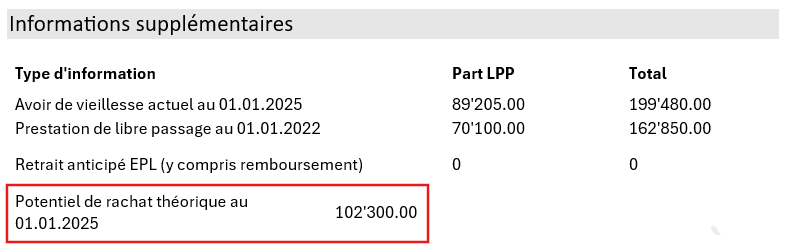

How much can I buy back?

The maximum amount you can buy back is determined by the difference between your retirement savings theoretical and your credit current in the pension fund. This difference represents your pension gaps, i.e. the capital you would have accumulated if you had always been affiliated to the same fund, with a constant and uninterrupted salary.

The redeemable amount is shown on your pension certificate:

Disadvantages of a buyback

1. Blocking funds

If you are considering withdrawing your 2nd-pillar assets in the near future, particularly for:

- A property purchase through the encouragement of home ownership (EPL),

- A final departure from Switzerland outside the EU/EFTA,

- A self-employed business

It is imperative that you have not made a buy-in within the previous 3 years. Otherwise, the tax authorities may retroactively claim the taxes saved through that buy-in, nullifying any tax benefit. However, this waiting period does not apply if you receive your retirement as an annuity. Therefore, if a withdrawal is planned in the medium term, postpone the buy-in or make it at least three years in advance.

2. Risk of under-coverage

A buy-in only makes sense if the pension fund is financially sound, meaning it has a coverage ratio above 100%. If the fund is underfunded (below 100%), it may implement restructuring measures that also affect the buy-in amounts (reduced benefits, lower conversion rate, etc.).

It is therefore advisable to ask your employer or the insurance company directly for the current level of cover, and to avoid buying out in the event of a persistent financial imbalance.

3. Limited impact on survivors' pensions

In many pension plans, disability and survivors' pensions are calculated on a lump-sum basis in percentage of the insured salary, not the accumulated capital. This means that the purchase will have no effect on these benefits.

If your priority is protecting your loved ones, consider a 3rd pillar or a complementary life insurance, which may be better suited.

Buyback in the event of divorce

In Switzerland, the law provides that in the event of divorce, occupational pension assets (2nd pillar) acquired during the marriage must be fairly divided (Art. 122 CC). This buy-in is not subject to the 3-year waiting rule for withdrawals. In short, this means:

- One person's pension fund transfers part of his BGV capital to the other's, in order to balance future pensions.

- Whoever gives up part of his or her assets suffers a reduction of its retirement capital.

The spouse whose LPP capital was reduced following the transfer may, if they wish, buy back the transferred amounts in order to restore their level of pension coverage.

Buy back years of contributions with a Pillar 3a withdrawal

The Swiss pension system allows you to use the assets accumulated in your pillar 3a to finance a buy-in to your pension fund (2nd pillar). This operation is tax-neutral and can be carried out until the statutory retirement age, or up to 5 years later if you are still working.

You can transfer all or part of your 3a capital to your pension fund, provided that the balance does not exceed the maximum buy-in amount. However, you will need to pay capital benefits tax (one-fifth of the regular tax rate, reduced and separate from income tax).

Pension fund purchase VS 3a contribution

A buy-in to the 2nd pillar allows you to fill contribution gaps with substantial amounts and offers a very advantageous tax deduction. However, any lump-sum withdrawal within three years following a buy-in may result in the loss of the tax benefit.

The 3rd pillar A, on the other hand, is more flexible. It allows for regular retirement savings with an annual deduction limit. It is accessible to everyone, including the self-employed, and offers early withdrawal options similar to the 2nd pillar. It exists in the form of accounts or funds, with higher return potential than the 2nd pillar but also greater risk. If you have already contributed the maximum to your 3rd pillar A, it is wise to make buy-ins to your pension fund.

Can I increase my buy-in potential?

If your new employer offers a more generous pension plan, your buy-in potential automatically increases. You can then buy in the difference between the benefits of the old and the new plan.

An increase in your insured salary raises the basis for calculating your contributions, as well as the maximum theoretical capital you could have accumulated. This expands the possible buy-in margin.

In the basic plans, often only one percentage of salary is insured (e.g. up to CHF 100,000). If you receive CHF 200,000, but only CHF 100,000 is included in the plan, you leave a potential of unused redemption. For incomes above CHF 132,300 (in 2026), it is possible to set up a supplementary plan or a separate plan 1e.

EPL repayment: Prerequisite for deductible redemption

If you have already used your 2nd pillar to finance the purchase of your primary residence through the home ownership encouragement (EPL), this situation directly affects your ability to make new tax-deductible buy-ins.

The mandatory prepayment rule

As long as you have not fully repaid an early EPL withdrawal, you cannot make tax-deductible buy-ins into your 2nd pillar. This rule is designed to prevent insured persons from simultaneously using their pension assets for home ownership while benefiting from tax advantages through buy-ins.

Specifically, if you withdrew CHF 80,000 from your 2nd pillar in 2015 to purchase your home, you must repay these CHF 80,000 before making a buy-in that will be recognized as tax-deductible by the tax authorities.

How EPL refunds work

There are two ways of repaying an advance withdrawal for the purchase of a home:

Voluntary repayment: You can voluntarily repay all or part of the withdrawn amount at any time, up to 3 years before the statutory retirement age (currently up to 62 for men and 61 for women). The repayment can be:

- Total: you repay the entire withdrawal

- Partial: you pay back part of the amount, but this does not yet entitle you to make tax-deductible buy-backs

Frequently asked questions

Yes, buy-ins into the 2nd pillar are fully deductible from taxable income at the federal, cantonal, and municipal levels, in accordance with Article 33 of the Federal Direct Tax Act (LIFD). This deduction applies without an annual limit, unlike pillar 3a. The buy-in amount directly reduces your taxable base in the year of payment.

For example, if you earn CHF 100,000 and buy back CHF 25,000, your taxable income falls to CHF 75,000, generating immediate tax savings of between CHF 6,000 and CHF 11,000, depending on your canton and family situation.

The tax saving generated by a buy-in typically represents between 25% and 45% of the amount contributed, depending on three main factors: your marginal tax rate, your canton of residence, and your family situation. The higher your income, the greater the savings, as you are taxed in higher brackets.

The tax deduction applies in the calendar year in which you make the payment. If you pay CHF 30,000 in November 2025, you will deduct this amount in your 2025 tax return, which you will file in spring 2026. To optimize your deduction, ensure that the payment is actually credited to your pension fund account before December 31.

Yes, absolutely. If you have already made an early withdrawal for the home ownership encouragement (EPL), you must fully repay this amount before being allowed to make new tax-deductible buy-ins. As long as the repayment is not complete, any buy-in you make will not be recognized by the tax authorities.

Anyone affiliated with a Swiss pension fund who has a contribution gap can make a buy-in. Limitations exist for individuals who are affiliated with a Swiss pension fund for the first time.

No, buy-ins into the 2nd pillar are always voluntary. Your employer cannot force you to make a buy-in. These are your personal funds that you voluntarily contribute to your pension fund to cover your pension gaps.

Warning: Do not confuse voluntary buy-ins with remedial contributions that some underfunded pension funds may temporarily impose. These remedial contributions are mandatory and shared between employer and employee, but they are also tax-deductible.

Yes, like any 2nd-pillar assets, it is taxed at the time of withdrawal (either as a lump sum or included in the pension). However, the taxation remains favorable because a reduced rate applies for lump-sum withdrawals.

Yes, but:

Withdrawal from 3a is imposed immediately.

This transfer is tax-neutral, unless you have a high income allowing a real deduction.