| Annual income (CHF) Jahreseinkommen |

Old-age/disability pension Alters-/Invalidenrente |

Widows/Widowers Witwen/Witwer |

Supplementary pension Zusatzrente |

Child's pension Kinderrente |

Orphan's pension Waisenrente |

Orphan's pension 60% Waisenrente 60% |

|---|---|---|---|---|---|---|

| bis 15'120 | 1'260 | 1'512 | 1'008 | 378 | 504 | 756 |

| 16'632 | 1'293 | 1'551 | 1'034 | 388 | 517 | 776 |

| 18'144 | 1'326 | 1'591 | 1'060 | 398 | 530 | 795 |

| 19'656 | 1'358 | 1'630 | 1'087 | 407 | 543 | 815 |

| 21'168 | 1'391 | 1'669 | 1'113 | 417 | 556 | 835 |

| 22'680 | 1'424 | 1'709 | 1'139 | 427 | 570 | 854 |

| 24'192 | 1'457 | 1'748 | 1'165 | 437 | 583 | 874 |

| 25'704 | 1'489 | 1'787 | 1'191 | 447 | 596 | 894 |

| 27'216 | 1'522 | 1'826 | 1'218 | 457 | 609 | 913 |

| 28'728 | 1'555 | 1'866 | 1'244 | 466 | 622 | 933 |

| 30'240 | 1'588 | 1'905 | 1'270 | 476 | 635 | 953 |

| 31'752 | 1'620 | 1'944 | 1'296 | 486 | 648 | 972 |

| 33'264 | 1'653 | 1'984 | 1'322 | 496 | 661 | 992 |

| 34'776 | 1'686 | 2'023 | 1'349 | 506 | 674 | 1'011 |

| 36'288 | 1'719 | 2'062 | 1'375 | 516 | 687 | 1'031 |

| 37'800 | 1'751 | 2'102 | 1'401 | 525 | 701 | 1'051 |

| 39'312 | 1'784 | 2'141 | 1'427 | 535 | 714 | 1'070 |

| 40'824 | 1'817 | 2'180 | 1'454 | 545 | 727 | 1'090 |

| 42'336 | 1'850 | 2'220 | 1'480 | 555 | 740 | 1'110 |

| 43'848 | 1'882 | 2'259 | 1'506 | 565 | 753 | 1'129 |

| 45'360 | 1'915 | 2'298 | 1'532 | 575 | 766 | 1'149 |

| 46'872 | 1'935 | 2'322 | 1'548 | 581 | 774 | 1'161 |

| 48'384 | 1'956 | 2'347 | 1'564 | 587 | 782 | 1'173 |

| 49'896 | 1'976 | 2'371 | 1'580 | 593 | 790 | 1'185 |

| 51'408 | 1'996 | 2'395 | 1'597 | 599 | 798 | 1'197 |

| 52'920 | 2'016 | 2'419 | 1'613 | 605 | 806 | 1'210 |

| 54'432 | 2'036 | 2'443 | 1'629 | 611 | 814 | 1'222 |

| 55'944 | 2'056 | 2'468 | 1'645 | 617 | 823 | 1'234 |

| 57'456 | 2'076 | 2'492 | 1'661 | 623 | 831 | 1'246 |

| 58'968 | 2'097 | 2'516 | 1'677 | 629 | 839 | 1'258 |

| 60'480 | 2'117 | 2'520 | 1'693 | 635 | 847 | 1'270 |

| 61'992 | 2'137 | 2'520 | 1'710 | 641 | 855 | 1'282 |

| 63'504 | 2'157 | 2'520 | 1'726 | 647 | 863 | 1'294 |

| 65'016 | 2'177 | 2'520 | 1'742 | 653 | 871 | 1'306 |

| 66'528 | 2'197 | 2'520 | 1'758 | 659 | 879 | 1'318 |

| 68'040 | 2'218 | 2'520 | 1'774 | 665 | 887 | 1'331 |

| 69'552 | 2'238 | 2'520 | 1'790 | 671 | 895 | 1'343 |

| 71'064 | 2'258 | 2'520 | 1'806 | 677 | 903 | 1'355 |

| 72'576 | 2'278 | 2'520 | 1'822 | 683 | 911 | 1'367 |

| 74'088 | 2'298 | 2'520 | 1'839 | 689 | 919 | 1'379 |

| 75'600 | 2'318 | 2'520 | 1'855 | 696 | 927 | 1'391 |

| 77'112 | 2'339 | 2'520 | 1'871 | 702 | 935 | 1'403 |

| 78'624 | 2'359 | 2'520 | 1'887 | 708 | 943 | 1'415 |

| 80'136 | 2'379 | 2'520 | 1'903 | 714 | 952 | 1'427 |

| 81'648 | 2'399 | 2'520 | 1'919 | 720 | 960 | 1'439 |

| 83'160 | 2'419 | 2'520 | 1'935 | 726 | 968 | 1'452 |

| 84'672 | 2'439 | 2'520 | 1'951 | 732 | 976 | 1'464 |

| 86'184 | 2'460 | 2'520 | 1'968 | 738 | 984 | 1'476 |

| 87'696 | 2'480 | 2'520 | 1'984 | 744 | 992 | 1'488 |

| 89'208 | 2'500 | 2'520 | 2'000 | 750 | 1'000 | 1'500 |

| 90'720+ | 2'520 | 2'520 | 2'016 | 756 | 1'008 | 1'512 |

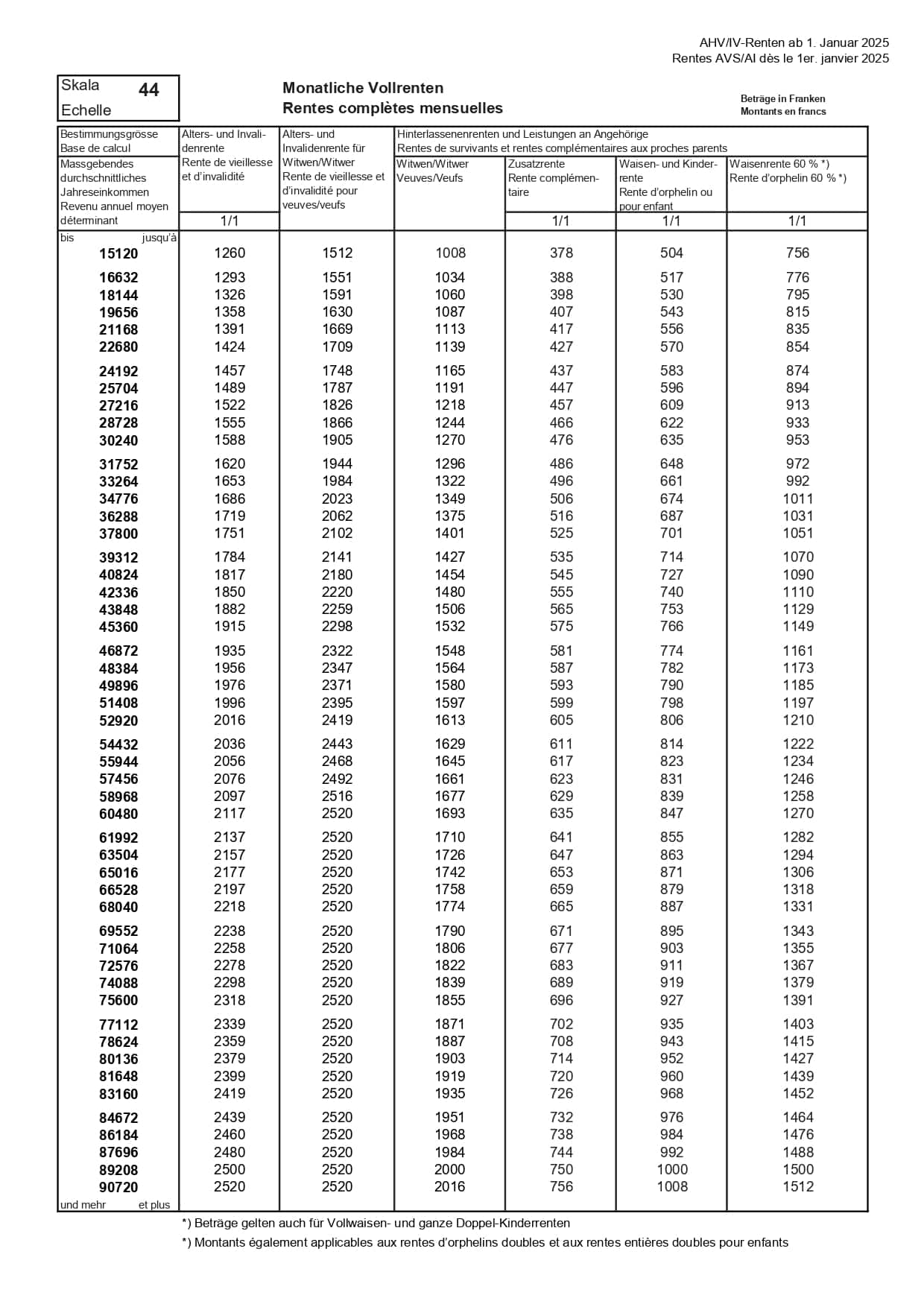

Scale 44 is the official scale used by AHV/OASI (Old-Age and Survivors' Insurance) to determine the amounts of AHV/OASI pensions and DI in Switzerland. This scale establishes a precise correspondence between an insured person's determining average annual income and the monthly amount of their pension. In effect since January 1, 2025, the current scale 44 applies to all old-age and disability pensions, as well as pensions for widows, widowers, orphans, and children.

The scale 44 system guarantees equitable redistribution: people who have contributed on higher incomes receive proportionally larger pensions, within the ceiling limit set by law.

In 2026, according to scale 44, the maximum AHV pension in 2026 is CHF 2,520 per month, or CHF 30,240 per year. This amount is awarded to people who have contributed without interruption throughout their working lives and whose average annual qualifying income is at least CHF 90,720.

The minimum pension, for its part, is set at CHF 1,260 per month for people with a complete contribution period but an average income below CHF 15,120.

For married couples, scale 44 provides for a ceiling: the total amount of the two pensions cannot exceed 150 % of the maximum individual pension. In 2026, this corresponds to CHF 3,780 per month (or CHF 45,360 per year) for the couple.

This cap applies even if each spouse would individually be entitled to the maximum pension of CHF 2,520. If the sum of the two pensions exceeds CHF 3,780, it is automatically reduced to comply with this limit.

The determining average annual income is the central element of the calculating an AHV pension according to scale 44. Here's how it works:

1. Summation of income: All earnings subject to AHV contributions during working life are added together, from the age of 20 until retirement age (64 for women, 65 for men).

2. Revaluation: These incomes are updated in line with wage trends in Switzerland, to take account of inflation and economic growth.

3. Bonuses: Additional amounts are added for years spent raising children under the age of 16 (bonuses for educational tasks) or caring for dependent relatives (bonuses for assistance tasks).

4. Average calculation: The total is divided by the number of years of contributions to obtain the average annual income.

This average income is then used to determine the pension amount according to scale 44. The higher the average income, the higher the monthly pension, up to a maximum of CHF 2,520.

Although scale 44 defines the AHV/OASI amounts, a comfortable retirement in Switzerland requires income higher than the maximum AHV/OASI pension. We estimate that a retirement income of approximately 70 to 80% of the last salary is necessary to maintain one's standard of living.

For a single person, this could represent between CHF 4,000 and CHF 6,000 per month, combining AHV/OASI (1st pillar), the pension fund (2nd pillar) and private savings (3rd pillar). For a couple, a combined monthly income of CHF 6,000 to CHF 8,000 is often considered comfortable. However, it should be noted that the higher the income, the greater the gaps will be, as the mandatory benefits of AHV/OASI and LPP are capped. Therefore, effective retirement planning is required in order to supplement income.

Yes, it is possible to advance the payment of the AHV/OASI pension, but this results in a permanent reduction of the amount according to scale 44. Insured persons can request their pension up to two years before the ordinary retirement age, i.e., from age 63.

The reduction is 6.8% per year of early withdrawal. For example, a person advancing their pension by two years will see their amount reduced by 13.6% for life. This reduction applies to the amounts defined by scale 44.

Conversely, it is also possible to defer payment of the pension for up to five years after ordinary retirement age, thereby increasing the amount of the pension.

The distinction between full and maximum pensions is essential to understanding scale 44.

A full pension means an annuity calculated on the basis of a full contribution period, In other words, there is no gap between the age of 20 and the normal retirement age (64 for women, 65 for men in 2026). A person receiving a full pension has contributed for 44 or 45 consecutive years. However, the amount of a full pension can vary considerably depending on the average annual qualifying income: it can be as low as CHF 1,260/month (minimum full pension) or as high as CHF 2,520/month (maximum full pension).

A maximum pension, corresponds to the highest amount that a person can receive under scale 44, i.e. CHF 2,520 per month in 2026. To obtain this maximum pension, two conditions must be met: a full contribution period AND an average annual income of at least CHF 90,720.

In a nutshell: all maximum pensions are full pensions, but not all full pensions are maximum pensions. A person may have paid contributions for 44 years without interruption (full pension) but receive only CHF 1,500/month if his income was modest, while another who has paid contributions for the same number of years on a higher income will receive the maximum pension of CHF 2,520/month.

The compensation fund enables’anticipating retirement between 1 month and 2 years at the most. This corresponds to an earliest departure of 62 years old for women born between 1961 and 1969, and 63 years old for the remaining policyholders.

You can calculate your AHV retirement pension yourself on the basis of your average annual qualifying income and scale 44, reduced by the percentage corresponding to anticipation:

Make a free appointment with one of our financial planning experts for personalized advice.

{kind=link}