")

AXA offers 4 funds for SmartFlex products:

1. AXA (CH) Strategy Fund Global Equity CHF (TER: 0.13%)

2. AXA (CH) Strategy Fund Swiss Equity CHF (TER: 0.37%)

3. AXA (CH) Strategy Fund Trends Equity CHF (TER: 0.34%)

4. AXA (CH) Strategy Fund Sustainable Equity CHF (0.24%)

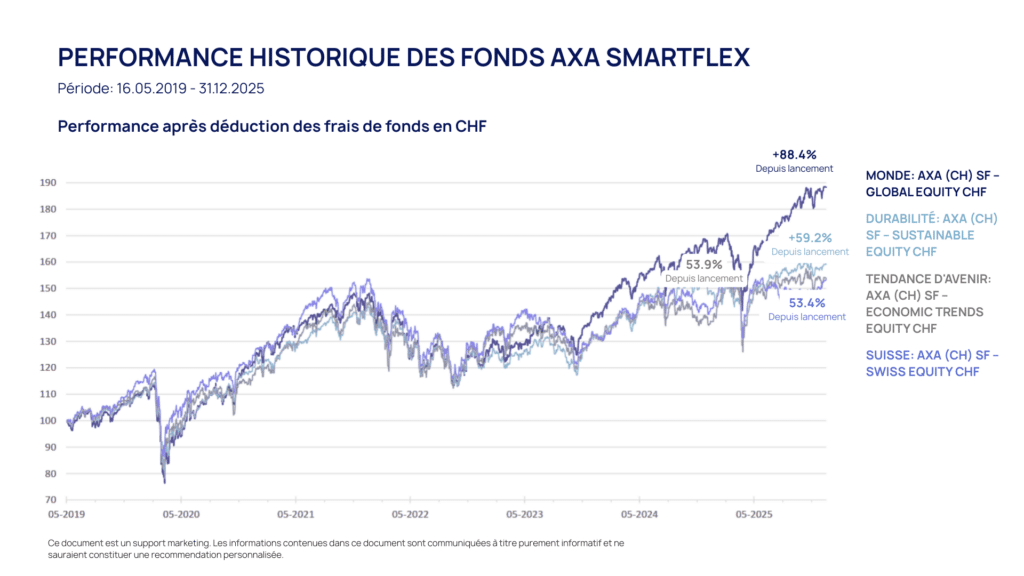

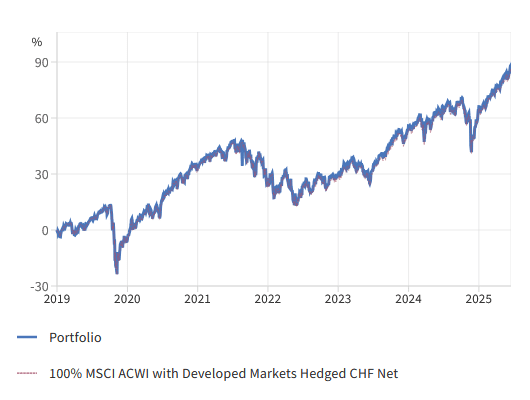

The best-performing funds is the historical Global Equity CHF (1), a passively managed global index fund that replicates the MSCI ACWI, hedged in Swiss francs at around 85 % against currency risks. The TER (annual costs) amounts to only 0.13%. Performance since launch in 2019 amounts to +87.72%.

AXA can be contacted at 0800 809 809 (Switzerland) or via the myAXA portal.

AXA’s 3rd pillar is aimed at anyone looking to build capital over the long term while benefiting from a favorable tax framework.

It is particularly well suited for those who wish to prepare for retirement proactively, protect their loved ones in the event of death, or simply invest in a disciplined way. Thanks to its flexibility, SmartFlex adapts equally well to young professionals, self-employed individuals, or families seeking a balance between security and performance.

The difference between 3a and 3b is as follows:

- Pillar 3a is linked to occupational pension provision: deposits are tax-deductible, but withdrawals are restricted by law (retirement, property purchase, independence, etc.).

- Pillar 3b, However, the money remains accessible at all times, and some solutions (such as SmartFlex 3b) offer inheritance benefits and protection in the event of bankruptcy.

In all cases, compare the 3rd pillars will help you find the solution that's best for you.

Returns depend on the proportion invested in yield-oriented capital (equities) and the investment theme chosen. Historically, SmartFlex funds have posted solid performances: the «World» theme, for example, has generated 87.72% in returns (+10% annualized) since its launch in 2019. This fund has even outperformed its benchmark of 86.27. Naturally, results vary according to market and investment horizon.

Absolutely. You can switch from one theme to another, for example from «World» to «Sustainability», free of charge, at any time.

The minimum annual premium is around CHF 600 for versions 3a and 3b. For the SmartFlex income plan, the initial contribution must be at least CHF 15,000.

Historically, equity investments have delivered higher long-term returns than so-called “safe” assets such as bonds or savings accounts. If you have more than 15 to 20 years before retirement, allocating a portion to equities is often recommended to generate stronger returns.

The key is to adjust the allocation to your risk profile and gradually reduce the equity portion as you approach retirement.

In the event of a loss of earning capacity, AXA provides a premium waiver.

In practical terms, if you become unable to work due to illness or an accident, AXA steps in and continues paying the premiums on your behalf, ensuring that your retirement plan remains fully intact.

It works as follows:

- As soon as a loss of earning capacity of at least 25% is recognized, AXA covers a portion of the premiums.

- If the disability reaches 66 % or more, you are completely free of premium payments.

- The waiting period before coverage begins depends on the contract (3, 6, 12, or 24 months, depending on your selection).

During this period, your SmartFlex plan continues to function normally: savings remain invested, guarantees remain in force, and you do not lose your tax benefits or your protection in the event of death.