Why should cross-border commuters think about additional savings?

Income from 1st and 2nd pillars are not enough to maintain a standard of living after retirement, especially for those who have not worked exclusively in Switzerland. The 3rd pillar represents an essential compensation tool. In addition, it offers the possibility of investing in a variety of vehicles, some of which guarantee capital security.

Types of 3rd pillar in Switzerland

In Switzerland, there are two types of third-pillar pensions: the tied personal pension (3rd pillar A)and the unrestricted individual pension plan (3rd pillar B).

Pillar 3A (restricted pension plan)

The Pillar 3a is designed specifically for retirement. The funds paid into it can only be recovered at the time of retirement or under certain conditions. exceptional situations (purchase of principal residence, permanent departure from Switzerland, etc.).

Payments are deductible of taxable income, subject to compliance with certain conditions, in particular for cross-border commuters (for example, the choice of cross-border commuter status). quasi-resident in some cases).

Pillar 3a contribution limits

In 2026, it will be possible to pay out the following amounts in tied personal pension plans:

- Employees affiliated to a pension fund: Up to CHF 7,258 / year

- Self-employed or employees not affiliated to a pension fund: 20% of income, maximum CHF 36,288

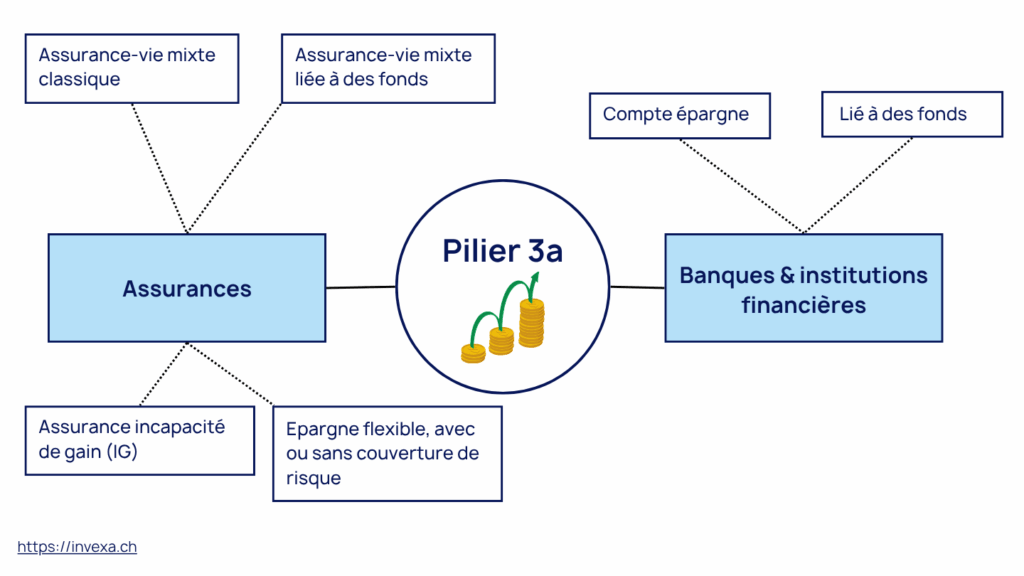

The 3rd Pillar A is divided into two categories: in banking and insurance. In insurance, we find classic life insurance (pure risk) or mixed (part of savings in funds or interest-bearing account), but also disability insurance, essential for the self-employed. Increasingly, insurance companies are also offering life insurance contracts. more flexible tied pension planssimilar to the 3a banks, but which offer covers (e.g. waiver of premiums in the event of disability, profit sharing, guarantees, etc.).

3a banking offers a more simple and flexibleThis type of account allows you to pay in the amount you want each year. Essentially, there are two possible forms: the interest-bearing account, linked to a investment funds. No additional coverage is available.

| Criteria | 3A insurance | 3A bank |

|---|---|---|

| Payment frequency | Determined in advance | Flexible |

| Type of investment |

|

|

| Surplus earnings | Profit sharing | No profit sharing |

| Possible coverage |

|

No |

| Bankruptcy guarantee | Amount guaranteed to 100% | Guaranteed amount up to CHF 100,000 |

| Waiver of premiums in the event of disability | Possible | No |

| Investment horizon | Long-term only | Medium to short term |

| Share of guaranteed capital | Possible | No |

| Pledging | Possible | Possible |

| Key benefits |

|

|

What strategy should you choose in 2026? Many cross-border workers open a basic health insurance plan for social protection and top up the remaining amount of the cap (CHF 7,258) via a bank account in order to maximize returns and flexibility.

Pillar 3B (unrestricted pension plan)

Unlike the 3A, the 3B is not designed exclusively for retirement. It offers great freedom in the use of funds, which can be mobilized for a variety of projects or financial needs. When we talk about 3B, we mean all the instruments that are not included in the 1st, 2nd and 3rd pillar A. These may include life insurance, classic cars, savings accounts, stocks or bonds, real estate, or even a life insurance contract. life annuity.

Contributions are not capped, allowing everyone to adjust their savings according to their financial situation and personal objectives. 3B offers a number of tax advantages, includingtax exemption on lump-sum benefits on withdrawal (if the pension provision is fulfilled), as well as income tax of only 4% for single-premium life annuities.

Tax deductions in pillar 3b: Contributions to a pillar 3b (life insurance only) are also tax-deductible in the canton of Geneva (single person: CHF 2,345/year) and Fribourg (single person: CHF 750/year).

New in 2026: Buyback of past contributions (3a buyback)

Since January 1st, 2026 (for the 2025 tax year), a major reform allows insured individuals to make up for years in which they were unable to contribute the maximum amount to their 3rd pillar. This measure is particularly beneficial for cross-border workers who started their careers in Switzerland later or who did not previously have quasi-resident status.

Key points to remember:

- Frequency: You can make a buyback every ten years.

- Deduction condition: To deduct this buyback from your taxes in 2026, you must strictly meet the conditions of quasi-resident status (90% of worldwide income taxed in Switzerland) in the year of the buyback.

- Justification: The buyback amount is limited by your pension “gap” (the difference between what you could have contributed and what you actually contributed in the past).

- Before making a large contribution, request a certificate of your past contributions from your pension provider in order to accurately calculate your buyback entitlement.

Conditions for taking out a 3rd pillar

For a cross-border worker, access to the 3rd pillar, particularly the tied pension plan (3a), is based on a key condition: quasi-resident status.

Quasi-resident status in Geneva and Fribourg (2026)

Quasi-resident status is the key that unlocks tax deductions for the 3rd pillar. Without it, your 3a contributions do not reduce your taxes.

The 90% rule in 2026: To be eligible, 90% of your household’s global gross income (including your spouse’s income in France, your rental income, or your dividends) must be taxable in Switzerland.

Warning regarding remote work: If you work more than 40% of your time from France (outside of specific agreements), you risk falling below the 90% threshold and losing your tax deductions.

Procedure: Application for Subsequent Ordinary Taxation (TOU)

- Deadline: You have until March 31 of the following year (e.g., March 31, 2027 for your 2026 income) to file the DRIS/TOU form.

- Irreversibility Once you request a TOU, you cannot go back to the current year, even if the final calculation turns out to be less advantageous than the flat-rate schedule.

- Deductible expenses: In addition to the 3rd pillar (CHF 7,258), the TOU allows you to deduct your childcare costs, alimony payments, 3b pillar contributions, and 2nd pillar (LPP) buy-ins.

To sum up, before taking out a 3rd pillar A, it is essential to check that your income from work in Switzerland is subject to contributions. AVSthat it meets the criteria for the quasi-residentin order to benefit from tax benefits. Moreover, quasi-resident status exists only in the cantons of Geneva and Fribourg.

On the other hand, a 3rd pillar B is open to all and offers a complementary savings solution without the constraints of tax status or payment ceilings, giving you the freedom to manage your portfolio for the future.

Since January 2021, cross-border workers can no longer request a correction of withholding tax through a subsequent ordinary taxation (TOU), which removes the tax deduction on their contributions. However, by obtaining quasi-resident status — conditional on 90% of the household’s income being taxed in Switzerland — it is possible to reduce taxable income by up to approximately CHF 7,258 per year per person.

Should I Contract a 3rd Pillar as a Cross-Border Worker?

The 3A pillar is above all a tax optimisation tool. It allows you to deduct the amounts paid in from your taxable income in Switzerland, making it a particularly attractive option for individuals subject to quasi-resident status (Geneva and Fribourg).

For cross-border workers employed in the cantons of Vaud, Neuchâtel, or Jura, the situation is different due to the bilateral tax agreements between Switzerland and France. In these cantons, cross-border workers are taxed in France rather than in Switzerland. They therefore do not pay withholding tax in Switzerland.

In this context, taking out a 3A pillar loses all its tax advantages.

Should I Forget about the 3A Pillar?

- Building long-term savings

- Providing a secure framework to plan your retirement

- Attractive returns depending on the chosen investment type

What 3rd Pillar Strategy to Use by Canton?

- Canton of Work

- Taxation

- Tax advantages of the 3a pillar

- Recommended strategy

- Geneva/Freiburg

- Other cantons

No (no deduction)

How can I take out a 3rd pillar as a cross-border commuter?

To open a 3rd pillar A as a cross-border commuter, you must be able to provide your G permit. medical questionnaire will be requested at the time of underwriting. Some insurance companies do not ask for a medical questionnaire if the insured is sufficiently fit. young. It is therefore advisable to open a 3rd pillar A account at an early stage.

Optimise your 3rd pillar

What 3rd pillar options are available for cross-border commuters?

In Switzerland, very few insurance companies accept cross-border commuters in the 3a category. Pillar 3a bank plans are, however, accessible to cross-border commuters in most cases.

Annual Tax Return: Your Obligations in France

- The form: Tick box 8UU on your income tax return (2042) and complete appendix 3916 (Accounts held abroad).

- What to declare: The name of the institution (e.g., UBS, VIAC, Swiss Life) and the account number. Annual interest from a 3a pillar is not taxable in France as long as it remains within the pension "tunnel."

- The fine: Failing to file your tax return correctly can incur a 1500 € fine per account even if you wouldn't have paid any tax on it.

Withdrawing your 3rd Pillar as a Cross-Border Worker: How to Avoid Double Taxation?

This is the number one fear of cross-border workers: will I be taxed twice when withdrawing my 3rd pillar? Once by Switzerland, and once by France?

The short answer is: no. The Franco-Swiss tax treaty is specifically designed to prevent this double taxation. However, the mechanism operates as an advance payment of taxes. If you do not follow the proper procedures, you could indeed lose money. Here’s exactly how the taxation works upon withdrawal.

Withholding tax levied by Switzerland (advance)

When you withdraw your capital (for retirement, purchasing a primary residence, or permanent departure), Switzerland does not pay you 100% of the amount.

The pension institution (your bank or insurance company) is legally obliged to withhold a withholding tax. This is not a penalty, but a guarantee for the state.

The rate of this tax does not depend on your canton of work, but on the canton where the foundation of your 3rd pillar is domiciled. (This is why many foundations are located in cantons with favorable tax regimes, such as Schwyz).

Obligation to inform in France

As a French tax resident, your worldwide income must be declared in France. Withdrawal of your 3rd pillar is no exception. In the year following your withdrawal, you must report this capital to the French tax authorities (via forms for income received abroad, such as 2047, and the standard 2042 tax return).

France will then apply its own taxation on this capital (a flat-rate levy of 6.75% on the capital, plus social contributions CSG/CRDS).

To avoid this dreaded double taxation, the Franco-Swiss bilateral treaty allows you to recover the full withholding tax that Switzerland deducted when you withdrew your 3rd pillar.

You have a period of 3 years after the payment of your capital to claim a refund of the Swiss withholding tax. After this period, the funds are permanently lost to the Swiss tax authorities.

Designing a savings strategy with the 3rd pillar

1. Define your goals

To begin with, it's essential to clearly define your savings objectives. This means identifying whether you simply want to build up savings for the future. retirement or if you also need to cover risks such as theearning incapacitythe deathor other financial contingencies. Once you've established your goals, you'll know whether you need a full coveragea simple funds savings plan or other solution to meet specific short- or medium-term needs.

2. Define your investor profile

Next, it is important to assess your investor profile in order toadapt your strategy to financial market fluctuations. To do this, you need to determine your risk tolerance and your investment horizon. An investor curator profile will prefer low-risk, moderate-return funds or a simple savings account, while a more dynamics could opt for more aggressive investments.

This personal analysis is essential for choosing products that match your needs. preferences and your situation current financial situation.

3. Compare funds and performance

Once your objectives and investor profile have been clearly defined, it's time to compare different offers available. This involvesanalysis performance historical and fees associated with 3rd pillar funds. You can compare the returns of guaranteed funds, unsecured funds and investment funds. actions or even solutions mixedkeeping in mind that the diversification remains an important lever for optimizing returns and limiting risks. A detailed comparative analysis will enable you to select products suited to your savings strategy.

4. Combining contracts

Finally, to maximize the tax benefits of the 3rd pillar, it may be wise to combine several contracts. Subscribing to several products allows you to make staggered withdrawals and therefore reduce your marginal tax ratetaxation.

Conclusion: What action should you take today?

The 3rd pillar for cross-border workers is not a “standard” product. It is a strategy that must be coordinated with your canton of work, your family situation in France, and your life plans.

In 2026, with the new contribution buyback options, the opportunity for optimisation has never been stronger. Whether you choose the flexibility of a bank or the protection of an insurance policy, the key is to start early in order to benefit from compound interest.

Frequently asked questions

Yes, cross-border commuters can take out a 3rd Pillar A, even if they live in France. This savings product is open to anyone working in Switzerland.

However, the Swiss tax advantage (deduction of payments from taxable income) is only available to cross-border commuters who have opted for quasi-resident status via T.O.U. (Taxation ordinaire ultérieure), i.e. in Geneva and Fribourg only.

Yes, but under conditions. Since 2021, only cross-border workers with quasi-resident status (more than 90% of their worldwide income earned in Switzerland) can deduct their 3a contributions from withholding tax. This mainly concerns workers in the cantons of Geneva and Fribourg.

The maximum deductible amount for an employee affiliated with a pension fund (2nd pillar) is CHF 7,258 per year. For self-employed individuals without a 2nd pillar, the limit is 20% of net income, up to a maximum of CHF 36,288.

Yes, but the benefit will not be tax-related in Switzerland because taxes are paid in France (according to the 1983 agreement). However, the 3rd pillar remains interesting for retirement savings, investment fund returns, and insurance coverage (death/disability), which is often more protective than in France.

You must report the existence of your account or contract each year using form 3916 (foreign accounts) and tick box 8UU on your 2042 income tax return. No tax is due on annual interest as long as the capital is not withdrawn.

Withdrawal is possible for three main reasons: reaching the legal retirement age, purchasing your primary residence (in France or Switzerland), or starting a self-employed activity.

Yes. The capital withdrawn is taxed in France, generally through a flat-rate levy of 6.75% (plus social contributions). The withholding tax deducted at source by Switzerland at the time of payment will be fully refunded once you provide proof of declaration to the French tax authorities.

The 3rd pillar supplements the 1st and 2nd pillars (AVS/AI and LPP) to maintain your standard of living in retirement.

- The pillar 3a (linked) is a locked-in savings up to 5 years before retirement, with tax benefits under certain conditions.

- The pillar 3b (free) offers greater flexibility and can be used as savings, life insurance or investment, with no payment limit.

From 2021The classic deductions linked to the 3rd pillar (and other expenses) are only possible for cross-border commuters with quasi-resident status (T.O.U), i.e. when 90 % of household income is taxed in Switzerland.

If you complete this condition, Pillar 3a contributions can be deducted from your Swiss taxable income, up to a maximum of CHF 7,258 per year in 2025. Otherwise, you won't benefit from any tax deduction, but you can still save freely in a 3b to prepare for your retirement.

3rd Pillar A funds can be withdrawn in the following ways following cases:

- Definitive departure from Switzerland,

- Transition to self-employment,

- Purchase or repayment of a main property,

- Purchase of 2nd pillar contributions,

- Retirement (up to 5 years before legal retirement age).

The withdrawal is subject to the capital benefits tax at a reduced rate. Funds from pillar 3b, on the other hand, can be freely withdrawn, subject to the conditions set out in the contract.

Thanks to the Franco-Swiss tax treaty, you do not pay tax twice. Switzerland withholds tax at source at the time of withdrawal, but you can request a full refund once you have proven that you declared it to the French tax authorities. Note: you only have 3 years to complete this procedure.