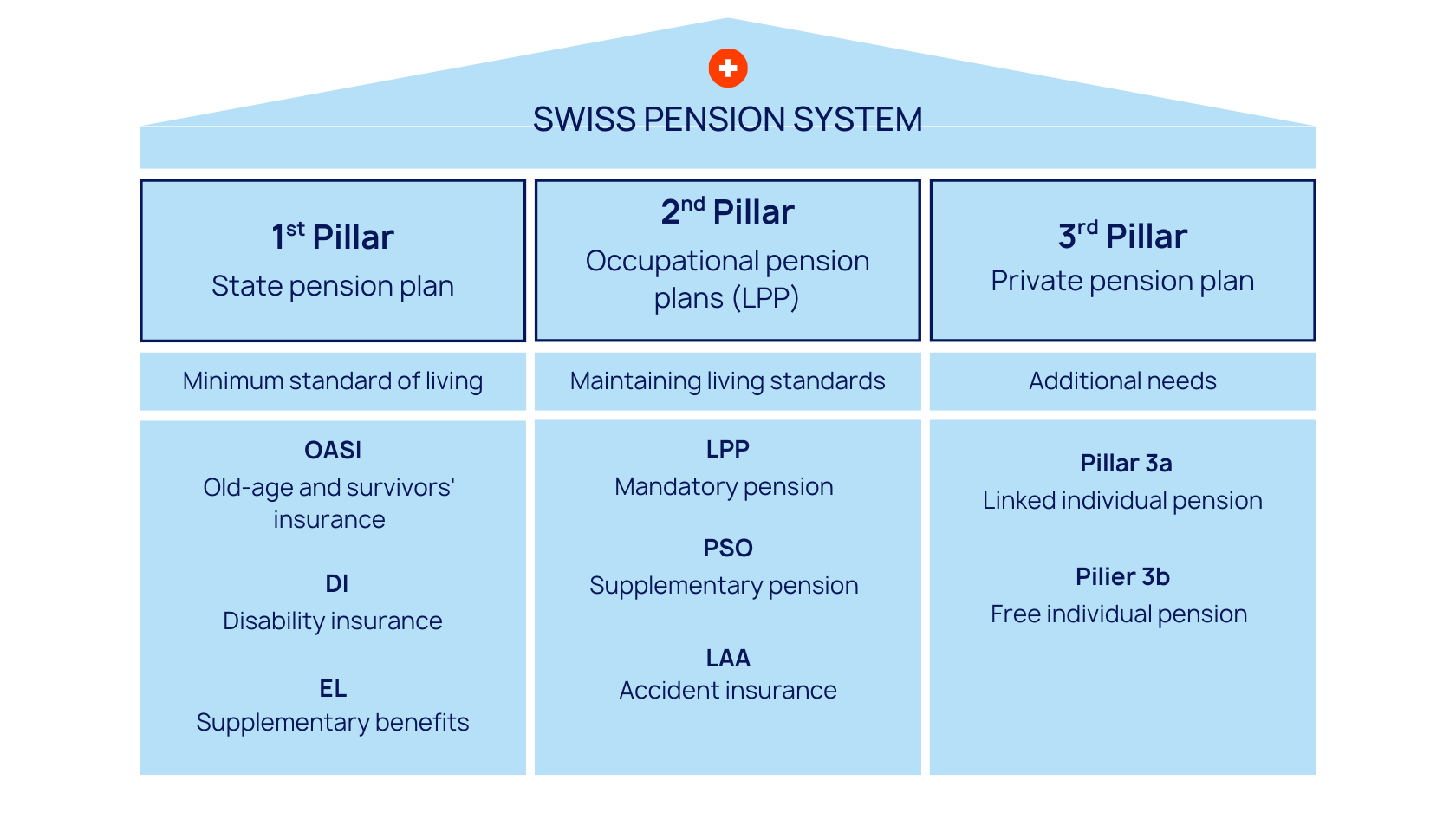

The 2nd pillar (BVG) in brief

- Mandatory at 17 years old (risks) and 25 years old (old age) for employees earning more than CHF 22,680/year

- Employer and employee shared contributions: The employer pays at least 50%

- Conversion rate: 6.8% of accumulated retirement savings

- Withdrawal possible in the form of an annuity, lump sum, or combination: irrevocable decision

- Early withdrawal allowed in 4 cases: Early retirement, real estate purchase, independence, permanent move from Switzerland

- Voluntary buybacks possible and tax-deductible

What is the 2nd pillar?

The 2nd pillar, also known as occupational pension or LPP (Law on Occupational Pensions), is a mandatory insurance system in Switzerland for employees whose income exceeds a certain threshold. It is part of the three-pillar system. Its purpose is to supplement the benefits of the AVS, ensuring a sufficient income in retirement, or in case of disability or death. Funded jointly by the employer and the employee, it is based on the principle of individual capital accumulation: each insured person saves for their own retirement.

Who is concerned?

Not all employees in Switzerland are automatically enrolled in the 2nd pillar. Mandatory affiliation depends on several conditions:

- Be employed and subject to AHV contributions

- Annual income over CHF 22,680 (threshold 2026)

- Must be at least 17 years old for death and disability insurance

- From the age of 24, start contributing to retirement too

LPP Thresholds (2026)

| LPP Setting | Amount |

|---|---|

| LPP entry threshold (minimum income) | CHF 22,680 |

| Coordination deduction | CHF 26,460 |

| Guaranteed minimum coordinated salary | CHF 3,780 |

| Maximum guaranteed coordinated salary | CHF 64,260 |

| Maximum Pensionable Salary | CHF 90,720 |

Even if you do not meet the standard conditions, it is possible to join the 2nd pillar on a voluntary basis. For example, an employer may choose to cover an employee whose income is below CHF 22,680. Likewise, self-employed individuals or those on short-term contracts can opt to contribute, although it is not mandatory. From age 24, contributions also start to build up savings for retirement.

Retirement contributions and bonuses

Contributions to the 2nd pillar (LPP) are calculated on the annual salary says coordinated (i.e. after deduction of a fixed amount known as the coordination deduction, CHF 26,460 in 2026). Contributions are shared between employer and employee, with the employer paying at least half (except for the self-employed, who must pay the full amount). Contributions comprise several components, including retirement savings, risks and expenses.

1. Old-age contribution

Retirement credits represent the savings portion of the occupational pension plan, and the interest rate on these credits is set by the employer. increases with age to gradually build up retirement savings. Here is an overview of retirement credits in 2026, depending on the age of the insured in the compulsory portion:

| Insured's age | Percentage % |

|---|---|

| 25 - 34 years old | 7% |

| 35 - 44 years old | 10% |

| 45 - 54 years old | 15% |

| 55 - 65 years old | 18% |

2. Risk premiums

Risk premiums finance the coverage against the risks of disability and death. This means that if an insured person becomes disabled or dies before reaching retirement age, the pension fund will pay a disability pension or a survivor’s pension (to the spouse, registered partner, or children). These premiums vary depending on age and gender.

3. Contribution to the LPP Guarantee Fund

Each pension institution must pay a contribution to the LPP Guarantee Fund, which secures the statutory minimum benefits in the event of a pension fund’s insolvency. This mechanism protects insured persons from losing their retirement savings if their fund goes bankrupt. The fund also intervenes in cases of restructuring or exceptional situations, such as fund mergers.

Benefits: Old Age, Disability, Death

The 2nd pillar also protects insured persons and their families against the risks of disability or death, as well as the inevitable risk of old age. Benefits are therefore paid out based on different life events, in the form of pensions. Here is a brief overview of the main benefits provided under the LPP:

| Type of pension | Details |

|---|---|

| Retirement | |

| Retirement pension | Paid starting at the legal retirement age. Calculated based on the accumulated retirement savings, at a conversion rate of 6.8%. |

| Retirement capital | You may withdraw one-quarter of your mandatory LPP balance as a lump sum. Some pension funds allow you to withdraw the entire balance. |

| Child benefit for retirees | 20% of the old-age pension paid per child, until the child turns 18 or 25 if the child is in school. |

| Disability before retirement | |

| Disability pension | If the insured person becomes disabled (as defined by the AI), they receive a pension calculated based on their accumulated balance plus future age-related adjustments, without interest. |

| Child disability allowance | 20% of the disability pension paid per child, until the child turns 18 or 25 if the child is in school. |

| Death before retirement | |

| Spouse's pension | The surviving spouse receives 60% of the pension if the marriage lasted at least 5 years and the spouse is at least 45 years old, or if there are dependent children. Otherwise, a lump-sum payment equivalent to 3 annual pensions may be paid. |

| Orphan's pension | 20% of the pension paid to each child until age 18, or age 25 if the child is in school. |

Annuity or lump sum: what to choose at retirement?

Upon retirement, you can receive your vested LPP (Occupational Pension Plan) benefits in the form of a lifelong annuity, a lump sum payment, or a combination of both. This choice is irrevocable and must be communicated to your pension fund at least one year in advance.

The Annuity guarantees a fixed monthly income for life, regardless of your lifespan or market fluctuations. With the statutory conversion rate of 6.8 % on the mandatory portion, it offers a guaranteed return that is difficult to match with safe investments. On the other hand, any remaining capital is not passed on to heirs, and the annuity is taxed at 100 % as income.

The capital It offers complete flexibility—paying off a mortgage, investing, planning an estate—and is taxed only once at a reduced rate upon withdrawal. However, you are solely responsible for managing the capital over 20 to 30 years, with no safety net if the funds run out.

The combination of the two is often the most balanced solution: a portion in annuity to secure a basic income, and a portion in capital for projects and inheritance.

For a numerical analysis, consult our LPP annuity or lump sum.

How can I improve my 2nd pillar benefits?

Performing buying into your pension fund is the most effective way toimprove your services from the 2nd pillar. These payments volunteers allow you to make up any contribution gaps, for example after a change of job, unpaid leave or a reduction in your working hours.

The amount purchased directly increases your retirement assets, which means a higher pension when you retire. In addition to this advantage, purchases are tax-deductible, which means you can reduce your taxable income. However, certain conditions must be met, including a three-year waiting period before a lump-sum withdrawal can be made if you have made a purchase.

To acquire optimize your pensionthe 3rd pillar offers a tailor-made solution that complements your pension fund. Visit Pillar 3a, and the pillar 3b in some cantons, benefit from a recognized tax advantage.

How do I withdraw my 2nd pillar?

The capital in your 2nd pillar can be withdrawn as follows certain conditions:

1. Retirement

You can request payment of all or part of your retirement capital in the form of a lump sum, in accordance with the rules of your pension fund. A formal request must be made several months in advance.

2. Permanent departure from Switzerland

If you leave Switzerland for a country outside the EU/EFTA, you can withdraw your entire 2nd pillar. If you are moving to an EU/EFTA country, only the amount in excess of your compulsory pension can be withdrawn, with some exceptions.

If you have already withdrawn your 2nd pillar upon leaving the country and are considering returning to Switzerland, the consequences for your retirement benefits are significant — find out more. Steps and available options.

3. Access to property

You can use your credit balance to finance the purchase of your principal residence, either by early withdrawal or as a guarantee (EPL - encouragement to home ownership).

4. Start of self-employed activity

5. Small amount

If your vested benefit credit is less than one year's contributions, you can apply to withdraw it.

Taxation of withdrawals

Each withdrawal is subject to the’capital gains tax, a tax on reduced rateseparate from ordinary income, to 1/5 tax rate. It is therefore advisable to plan this operation carefully.

Taxation of Withdrawals

In Switzerland, the withdrawal of LPP capital is subject to a capital gains tax, it is a tax distinct from ordinary income, applied at a reduced rate corresponding to approximately 1/5 of the usual rate depending on the cantons.

The rate varies significantly depending on the canton of residence at the time of withdrawal. For a withdrawal of CHF 200,000, the differences are significant:

| Canton | Estimated rate | Estimated tax |

|---|---|---|

| Zug | ~4,2% | CHF 8,400 |

| Valais | ~5,5% | CHF 11,000 |

| Zurich | ~5,6% | ~CHF 11,200 |

| Geneva | ~5,7% | CHF 11,400 |

| Fribourg | ~5,8% | CHF 11,600 |

| Vaud | ~6,4% | SF 12,800 |

The tax is progressive: The larger the amount withdrawn in a single instance, the higher the effective rate. Splitting withdrawals over several tax years can generate significant savings. For example, in Geneva, two withdrawals of CHF 250,000 spaced one year apart cost approximately CHF 10,500 less than a single withdrawal of CHF 500,000.

Three essential rules to remember:

- Never withdraw capital within 3 years of an LPP withdrawal, or face tax recall.

- Avoid accumulating the LPP withdrawal and the 3rd pillar withdrawal in the same tax year

- For couples, coordinating withdrawals over two distinct years

Special case of French cross-border workers: Withdrawals from the 2nd pillar are subject to several cumulative taxes: Swiss withholding tax, French taxation (a flat-rate levy of 7.5% after a deduction of 10%, or a progressive tax scale), and social security contributions (~9%). On a principal amount of CHF 200,000, the total tax burden can reach CHF 30,000 to 35,000, depending on the situation. Advance planning is essential.

For an accurate estimate of your taxes and an optimized withdrawal strategy based on your canton and family situation, consult our comprehensive guide on Swiss Pension Fund Withdrawal Taxation.

LPP Buyback: Optimize your retirement

Performing buying into your pension fund is the most effective way toimprove your services from the 2nd pillar. These payments volunteers allow you to make up any contribution gaps, for example after a change of job, unpaid leave or a reduction in your working hours.

The amount purchased directly increases your retirement assets, which means a higher pension when you retire. In addition to this advantage, purchases are tax-deductible, which means you can reduce your taxable income. However, certain conditions must be met, including a three-year waiting period before a lump-sum withdrawal can be made if you have made a purchase.

To acquire optimize your pensionthe 3rd pillar offers a tailor-made solution that complements your pension fund. Visit Pillar 3a, and the pillar 3b in some cantons, benefit from a recognized tax advantage.

Dividing the 2nd pillar in the event of divorce

In the event of divorce in Switzerland, the 2nd pillar assets accumulated during the marriage are in principle shared equally between the spouses, regardless of the division of assets or matrimonial property regime. This division concerns only the termination benefits (vested benefits) accrued during the couple's life together.

The amount is calculated as of the date on which the divorce proceedings are initiated. Each spouse is entitled to half pension assets saved by the other during the marriage. If one of the spouses has made little or no contributions (e.g., in the event of a career break to raise children), he or she can recover part of the other's assets in the form of a compensatory allowance.

The amount transferred is paid either into the beneficiary's pension fund or into a vested benefits accountif he is not immediately affiliated to a fund. There are exceptions (e.g. in the case of a different agreement validated by a judge, or where the pension is already in payment), but the principle of sharing remains the rule under Swiss law.

Freedom of movement and change of employment

A Liberty deposit account used for conserve your second pillar assets when leaving a pension fund without immediately joining another. It is a mandatory transitional solution to avoid losing your occupational benefits.

This situation arises in particular if you:

- Leave your job without taking a new one immediately

- Become self-employed

- Reduce your work rate below the LPP threshold

- Are unemployed for a period

- Move abroad

Having accumulated it, it remains blocked, protected, and continues to generate interest, while being exempt from wealth tax. You can transfer it to either a Bank account of free passage, either in a Insurance policy free passage. You thus maintain your link with the provident fund, pending a new affiliation or another event (retirement, repurchase, or early withdrawal under certain conditions). In all cases, compare free passage solutions is essential before making a decision.

Frequently asked questions

The 2nd pillar supplements the AHV and helps maintain approximately 60% income prior to retirement. It is financed by contributions shared between employee and employer.

The second pillar was introduced in Switzerland in 1985 with the entry into force of the LPP.

The average LPP old-age pension in Switzerland amounts to approximately CHF 100,000-150,000, but varies greatly depending on age, salary, and contribution period.

To the retirementor earlier in some cases: definitive departure from Switzerland, purchase of a home, start of self-employment or amount too low.

Every year, your pension fund sends you an annual pension certificate indicating your pension assets and expected benefits.

All 17 years old or more whose annual income exceeds CHF 22,680 (in 2025). The self-employed can join voluntarily.

You can unlock your 2nd pillar in Switzerland when you retire or earlier to buy a home, become self-employed or leave the country permanently.

What is the 2nd pillar?

The 2nd pillar is mandatory for employees whose annual income exceeds a minimum threshold (CHF 22,680 from 2025). Contributions are shared between the employee and the employer, and paid into a pension fund (pension fund). This savings system is based on the principle of capitalization: the contributions paid in are invested and generate personal assets.

Situations giving right to a withdrawal

Your BVG capital can be withdrawn under several conditions:

1. Ordinary retirement

The most common situation is withdrawal at the time of retirement. At the legal age (65 years for both men and women), the insured person can receive their assets in the form of a lifetime pension, a lump-sum payment, or a mix of both if allowed by their pension fund’s regulations. The insured is entitled to withdraw at least 25% of their capital.

The choice to receive all or part of the capital instead of a pension must be made in writing within a deadline set by the pension fund (often 1 to 3 years before retirement). Once this choice is made, it is irrevocable.

2. Early retirement

Most pension funds allow early retirement from 58 years old. In this case, the insured may request an early annuity (with a lower conversion rate), or a lump-sum payment in accordance with the terms of his or her regulations.

Some institutions impose a proportional reduction in benefits for each year of early retirement. In general, early retirement can reduce the conversion rate between 0.10 and 0.30% per year of anticipation.

3. Withdrawal for the purchase of a home as a principal residence

The Swiss Vested Benefits Act (LFLP) allows the use of 2nd pillar funds under the home ownership promotion scheme (EPL), meaning for the purchase, renovation, or repayment of the mortgage on your primary residence. Two options are possible:

- Early withdrawal: part or all of the equity can be used to finance the purchase, construction or mortgage repayment of a home for own use.

- Pledging: the capital remains in the pension fund but is pledged to the bank to increase borrowing capacity.

The property must be used as principal residence (and not as a second home or investment property). Withdrawals are subject to a one-off capital gains tax at a reduced rate.

4. Final departure from Switzerland

If the insured moves to a country outside the European Union or EFTA, they may withdraw their entire LPP assets (both mandatory and supplementary parts). However, if moving to an EU or EFTA country, only the supplementary assets can be withdrawn. The mandatory assets are transferred to a vested benefits account.

Proof of new residence abroad is required (certificate of residence, deregistration from the commune, etc.).

5. Starting a self-employed business

When a person leaves salaried employment to become self-employed, they can request the payment of their pension assets. This withdrawal is only possible within one year after the start of the self-employment activity and provided that this activity is not secondary.

Concrete evidence is required (AHV registration , tax status, etc.).

Second pillar withdrawal conditions for cross-border commuters

- The supplementary portion can be withdrawn freely as capital.

- The mandatory portion It must remain in a vested benefits account in Switzerland until the legal retirement age or until one of the withdrawal conditions is met.

Taxation of capital withdrawals

In Switzerland, capital withdrawn from the 2nd pillar is subject to a capital benefits tax. Upon withdrawal, the amount is taxed at a reduced rate, equivalent to one-fifth of the normal income tax rate. The tax is levied in the canton of residence at the time of payment, based on the statement provided by the pension fund to the tax authorities. For individuals residing abroad, the tax is withheld directly at source in Switzerland.

The amount of tax varies greatly from canton to canton. In Geneva and Lausanne, for example, a withdrawal of CHF 500,000 results in a tax of around CHF 39,000 to 42,000 for a single person. In Valais and Fribourg, the amounts may be slightly lower, but are still substantial. The higher the amount withdrawn, the higher the effective tax rate, due to the progressive nature of the tax scale.

It’s worth noting that voluntary buy-ins to the 2nd pillar, often made to optimize retirement savings, are tax-deductible. However, to keep this benefit, you must wait at least three years before withdrawing the capital, or you risk having to repay the tax deduction.

There are two common strategies for limiting withdrawal tax. The first is to stagger withdrawals over several years in order to benefit from a lower rate each time. The second is to take up residence in a canton with more favorable tax conditions in the year of withdrawal. Some cantons, such as Zug, Schwyz and Obwalden, offer much more favorable conditions than Vaud, Geneva or Neuchâtel.

Taxation of withdrawal for cross-border commuters residing in France

1. Withholding tax in Switzerland

At the time of disbursement, the provident institution deducts a reduced withholding tax. The rate depends on the canton where the provident foundation is domiciled, not on your canton of employment.

2. Taxation in France

- Flat-rate deduction of 7.5 % (after a 10 % allowance): Advantageous, definitive, and separate option from the rest of the income. It is irrevocable.

- Progressive scale: by default if the withdrawal is considered fractional. A quotient attenuation system is possible (only 1/4 of the capital is added to income, multiplied by 4), but remains less advantageous.

3. Social deductions

4. CMU/CNTFS Contribution (if applicable)

What that represents concretely

| Withdrawal | Estimated amount |

|---|---|

| Swiss withholding tax (e.g., Geneva) | 12,000 Swiss Francs |

| French flat-rate withholding tax (7.5% after deduction) | CHF 13,500 |

| French social security contributions (~9%) | CHF 6,000 – 7,000 |

| CMU Contribution (if applicable, with 2-year delay) | Variable |

| Estimated total | CHF 30,000 – 35,000 |

No double taxation thanks to the Franco-Swiss convention

The bilateral Franco-Swiss tax treaty is designed to prevent you from paying taxes twice. The withholding tax levied by Switzerland at the time of payment is fully refunded to you, provided you prove your declaration to the French tax authorities. You have a deadline of 3 years after payment to claim this refund. After this period, the funds are permanently lost.

Optimize withdrawal as a cross-border worker

Two main levers can reduce the tax burden:

Withdrawal timing: Prioritize withdrawal before definitively returning to France if possible, and avoid accumulating LPP withdrawals with other significant income in the same tax year.

Split withdrawals If you have vested benefits in addition to your occupational pension (LPP), withdraw them in separate tax years. Each withdrawal is taxed separately, which reduces the effective rate applied.

For a precise estimate of your taxation and an optimized withdrawal strategy according to your situation, consult our Comprehensive Guide to Withdrawing from Pillar 2.

How can I collect my BVG assets?

Occupational pension provision, or the 2nd pillar, aims to maintain the standard of living at retirement as a supplement to the AVS. Upon reaching retirement age, insured individuals can choose between a life annuity, a lump-sum withdrawal, or a combination of both, depending on the rules of their pension fund.

A lump-sum withdrawal offers greater flexibility: it allows you, for example, to invest, pay off a mortgage, or plan your estate. However, it also carries risks, notably the challenge of managing your savings over an uncertain lifespan. Before deciding, it’s crucial to understand how much you can withdraw, under what conditions, and the tax and inheritance implications.

How much can I withdraw in capital?

In Switzerland, according to the Federal Law on Occupational Retirement Provision (LPP), every insured person has the right to withdraw at least one quarter of their mandatory retirement savings as a lump sum, regardless of their pension fund’s regulations.

However, some pension funds offer the option of withdrawing more, or even all, of the accumulated capital, provided this is expressly provided for in their internal regulations. This right does not apply automatically to the entire capital.

A concrete example

Mr Doe reaches retirement age with a pension fund balance of CHF 400,000 (compulsory) and CHF 100,000 (supplementary). By law, he can withdraw at least CHF 100,000 (i.e. 1/4) in capital. If his pension fund regulations so permit, he may also choose to withdraw the entire CHF 500,000.

Should I withdraw my 2nd pillar capital for retirement?

The annuity may seem reassuring on paper, but it hides a reality: with a capital of CHF 400,000 and a conversion rate of 6.8%, you receive CHF 27,200 per year. This seems generous until you realise that it takes around 14 and a half years to recover your own capital.

The conversion rate is in freefall. In 6.8% (in the mandatory part only), it is artificially maintained by political constraints, but demographic projections are relentless: insurers will reduce it sooner or later. Reforms are already underway. If you retire in 5 or 10 years, there's no guarantee that this favorable rate will still be in effect for you.

You lose control of your money. By opting for the annuity, you permanently transfer your capital to the pension fund. In the event of premature death, a significant part of what you have built up disappears and does not go to your heirs. The withdrawn capital, on the other hand, becomes part of your assets, can be passed on, and remains available in case of unforeseen events.

Flexibility is highly valuable. Paying off a mortgage with released capital can sustainably reduce your fixed expenses, and mortgage interest remains tax-deductible, further improving the equation. You can also invest gradually, adapting your strategy to changing needs, rather than being locked into a rigid income stream.

Historically, a 36% return over 20 years is modest. That is less than 2% annualised — well below what a diversified portfolio has historically produced over such a long period. Saying that “replicating the annuity in the markets is difficult” is equivalent to saying you should not invest at all. Yet the data over a 20-year horizon clearly supports investing.

Of course, taking the capital withdrawal must be planned: taxation is lump-sum and separate from ordinary income, and a staggered withdrawal can significantly reduce the tax bill. But when well structured, it is often the option that gives you the most freedom, and freedom has a value that an annuity never compensates.

Need help choosing between a lump sum and an annuity?

How do I withdraw my 2nd pillar?

You must notify your intention to withdraw a lump sum well in advance—several months before your official retirement date. Each pension institution sets its own internal deadlines, but it is common for the formal request to be submitted at least six months before retirement. Missing this deadline may result in losing the right to a lump-sum payment, leaving only the option of receiving an annuity. The spouse’s consent (husband or wife) is required under the LPP.

How can I withdraw my vested benefit capital?

Withdrawing capital from a vested benefits account is possible at normal or early retirement age, in accordance with the terms of your vested benefits contract and within the scenarios defined by the LPP.

To make a withdrawal, you must submit a written request to your vested benefits institution. It is essential to provide all required supporting documents, which vary depending on the reason for the withdrawal. Additionally, it is important to note that vested benefits assets, like those in a pension fund, are subject to capital benefits tax at the time of withdrawal.

Frequently asked questions

Withdrawal from the 2nd pillar is possible in 5 cases:

- retirement (ordinary or early),

- purchase or construction of a principal residence / repayment of a mortgage,

- definitive departure from Switzerland,

- setting up a self-employed business,

- or, in some cases, a disability pension.

Yes, if you remain a member of a pension fund after the legal retirement age (e.g. by extending your working life), most regulations stipulate a limit of no later than 70 years old. After this age, only an annuity can be paid.

You must submit a written request to your pension fund or the vested benefits institution holding your assets. The request must be accompanied by the required supporting documents (proof of property purchase, certificate of independence, certificate of departure, etc.).

If you suspect that your vested benefits have been lost, you must submit a request to asset search to the Centrale du 2ème pilier.

The lump-sum withdrawal is taxed separately from your income, at a reduced and progressive rate. The rate depends on the canton, the amount withdrawn, and your marital status. Staggering withdrawals over several years or accounts can help optimize taxation.

Yes, but the withdrawn capital cannot be reintegrated into the pension fund. If you return to Switzerland, you will start contributing again based on your new income, like any new insured person, while having the option to make buybacks.

No. Withdrawal is allowed only for your primary residence — the one you personally live in. Secondary residences, rental properties, or investment assets are excluded.

You can usually apply for early withdrawal from the age of 58, depending on your pension fund regulations. Please note: this will permanently reduce your benefits, as the conversion rate falls for each year of early withdrawal.

In this case, only the supplementary portion of your BVG/LPP credit can be withdrawn. The compulsory portion is transferred to a vested benefits account in Switzerland, until you retire.

Yes, most pension funds allow a mixed withdrawal: one part in capital, the other in annuity. This choice must be announced in writing within the set timeframe (often 1 to 3 years before retirement).

Why should a self-employed person contribute to the second pillar?

In Switzerland, the law on occupational pensions (LPP) does not impose mandatory contributions for self-employed workers. This special status offers great cash flow flexibility but implies full responsibility: the self-employed individual must manage their own coverage in case of disability, death, and for retirement.

If the majority of freelancers and entrepreneurs prioritize Pillar 3a for self-employed individuals due to its flexibility, then the 2nd pillar optional proves to be extremely powerful for:

- Stable and high income (over CHF 100,000)

- Mass tax optimization via fully deductible contribution buy-backs.

- Lifetime annuity guarantee (annuity) to secure their old age.

Key Figures LPP (Calculation Bases)

| LPP Setting | Amount |

|---|---|

| LPP entry threshold (minimum income) | CHF 22,680 |

| Coordination deduction | CHF 26,460 |

| Guaranteed minimum coordinated salary | CHF 3,780 |

| Maximum guaranteed coordinated salary | CHF 64,260 |

| Maximum Pensionable Salary | CHF 90,720 |

What are the advantages of a 2nd pillar for the self-employed?

1. Massive tax deductions and pension fund buybacks

Ordinary contributions paid into the 2nd pillar are fully deductible from taxable income of the independent.

The real tax advantage lies in the Discharge share buybacks (LPP buybacks). If you have never contributed to the second pillar in the past, you have a potential «pension gap» of tens or hundreds of thousands of francs. You can inject these amounts to drastically reduce your tax bracket (federal, cantonal, and communal taxes).

2. A life annuity: psychological and financial security

One of the main advantages of the 2nd pillar compared to the 3rd pillar a is the life annuity.

- The risk of 3a: It is perceived as capital upon retirement. The self-employed individual must then manage it themselves and takes the risk of depleting their capital at an advanced age.

- The security of the 2nd pillar: The pension fund guarantees you a fixed monthly payment for the rest of your life, regardless of how long you live. Additionally, it includes survivor and orphan pensions.

3. Full protection against risks (Disability and Death)

- Disability pension from the Swiss Pension Fund calculated on the basis of the insured salary.

- A death benefit or an annuity for your loved ones.

For a freelancer, this avoids the need to take out multiple pure risk insurances (loss of income, 3b) from private companies: everything is centralized and optimized.

The disadvantages of occupational pensions (LPP) for the self-employed

- The amount of contributions (100% payable): Unlike an employee, whose employer pays at least half of the contributions, a self-employed person is responsible for both the employer’s share and the employee’s share. Depending on your age group, the financial burden ranges from 7 % to 18 % of the coordinated salary.

- Lack of flexibility: The second pillar is rigid. Contributions are contractually fixed according to the insurance plan. Unlike the 3a, you cannot decide not to contribute anything in a year when business is slower.

- The reduction of the 3a pillar ceiling: This is a crucial calculation. As soon as you enroll in a 2nd pillar plan, you lose the right to contribute to the "large 3a" (up to 20 % of net income, max. CHF 36'288). You then fall under the employee contribution limit (max. CHF 7,258).

Where to affiliate as a self-employed person for one's 2nd pillar?

- Your professional association's treasury: Sectors (doctors, lawyers, architects, fiduciaries, construction trades) have created dedicated pension funds. These are often the most advantageous and best suited to the realities of the profession.

- Your employees' cash box: If you employ staff and have opened a collective occupational pension (LPP) plan for your company, you can apply to join it personally under the same conditions.

- The LPP substituting institution foundation This is the legal fallback solution. It is obliged to accept any self-employed person affiliated with social security. However, the plans are very standardized (strict mandatory occupational pension) and generally offer less attractive returns for the supplementary portion.

Comparison: Pillar 2 vs. Pillar 3a for the self-employed

| Criteria | 2nd pillar (BVG) | 3rd pillar A |

|---|---|---|

| Affiliation | Optional, requires a fund that accepts self-employed individuals. | Open to all AHV insured individuals, easily accessible through banks or insurance companies. |

| Tax allowance (2025) | Deductible contributions (max. salary CHF 64,260). | Up to CHF 36,288/year if no 2nd pillar CHF 7,258/year if with 2nd pillar. |

| Investment | Generally standardized (guaranteed interest rate). | Wide selection (index funds, risk profiles, active/passive management). |

| Risk protection | Includes disability and death. | Optional depending on the chosen contract. |

| Retirement benefits | Life annuity primarily (option for partial lump sum). | Lump-sum capital contribution. |

| Buybacks and tax optimization | Yes: Tax-deductible buybacks. | Payouts possible from 2026 for 2025. |

| Ideal for | High income, need for guaranteed annuity and tax optimization. | Freelancers in the startup phase or seeking more flexibility. |

| Flexible payments | Low: contributions defined by the insured salary. | Assurance: annual adjustment Bank: no deposit requirement. |

Conclusion: What foresight strategy to choose?

- In the launch phase / Fluctuating revenues: Opt for a Pillar 3a account (without a Pillar 2 account). Take advantage of the 20% income limit to maximize your flexibility and invest in high-performing funds.

- Cruising phase / Stable and high income (> 100k): Affiliate with a 2nd pillar. Use ordinary contributions to lower your current taxes, keep the "small 3a" of CHF 7,258, and use your excess cash for deductible pension fund buy-ins.

FAQ – Frequently Asked Questions about the Independent Second Pillar

The Current Tax Rules

In Switzerland, the pension system is based on a consistent principle: during working life, contributions paid into the 2nd pillar (LPP) and the 3a pillar are deductible from taxable income. In return, the benefits received at retirement are subject to tax. However, the form of the payment—annuity or lump sum—determines how this tax is calculated, and that is precisely where everything is decided.

When an insured person chooses to withdraw their savings as a lump sum, the tax is not calculated according to the ordinary income tax scale. It is levied separately, at a reduced rate, generally corresponding to around one-fifth of the ordinary federal tax rate. This reduction reflects a simple economic reality: a lump-sum withdrawal is a one-off event, whereas an annuity is received over a lifetime and therefore naturally benefits from lower tax progression brackets.

This differentiated treatment is not a legislative oversight. It is a deliberate incentive for pension savings, consistent with the philosophy of the three-pillar system.

Planned Government Changes

As part of its budget relief programme, the Federal Council proposed to align the taxation of lump-sum withdrawals from the 2nd and 3rd pillars with that of annuities. In practical terms, this would have meant removing the reduced rate at the federal level: the amounts withdrawn would have been included in the calculation of ordinary taxable income, or subject to a significantly higher tax scale. The stated objectives were twofold.

On the one hand, to generate additional revenue for federal finances. On the other hand, to reduce what was perceived as a tax optimisation strategy accessible to high-income taxpayers, who make multiple LPP buy-backs to deduct significant amounts during their working life, then withdraw them at a reduced rate at retirement.

The anticipated economic consequences were significant: a potential tax increase of several thousand to several tens of thousands of francs depending on the capital accumulated, an expected shift away from lump-sum withdrawals in favour of annuities, and a risk of discouraging pension savings in general.

Refusal by Parliament

The proposal sparked broad, cross-party opposition. The central argument of the opponents was that it would be unacceptable to “change the rules mid-game.” Policyholders who had planned their retirement for decades and made LPP buy-backs based on a known tax framework would have seen their situation retroactively altered. The threat of a referendum was raised.

In December 2025, the State Counsel rejected the measure. In March 2026, the National Counsel also dismissed it. The tax increase has therefore been abandoned, at least in this form and within this legislative context.

For policyholders, the conclusion is clear: the tax rules applicable to lump-sum withdrawals remain unchanged for now. Withdrawals continue to be taxed at a reduced rate, separately from other income, without any increase in the federal tax scale.

What Is Not Changing

The rejection of this proposal does not mean that the taxation of lump-sum withdrawals is negligible. Quite the contrary. Significant differences in treatment remain depending on several variables that can be influenced.

Staggering withdrawals remains the most accessible optimisation lever. The tax authorities aggregate all withdrawals made within the same calendar year, including those of a spouse. The higher the amount withdrawn at once, the higher the effective tax rate becomes. Spreading withdrawals from the 3rd pillar, the 2nd pillar, and any vested benefits accounts over several tax years helps reduce this progressive effect.

Opening multiple 3a pillar accounts as early as possible, in order to be able to liquidate them in a staggered manner as retirement approaches. It is worth remembering that 3a pillar assets can be withdrawn up to five years before the official AVS retirement age.

The canton of residence at the time of withdrawal is also decisive. The differences between cantons are considerable. For a withdrawal of CHF 300,000 by a single person, the overall effective tax rate (federal + cantonal + communal) ranges from around 4.5% in the most tax-friendly cantons to nearly 9% in higher-tax cantons. This can represent a net difference of more than CHF 13,000 for the same capital. An early move to a tax-favourable municipality can generate substantial savings — provided that the change of residence is genuine and recognised by the tax authorities.

Voluntary buy-ins into the 2nd pillar remain fully deductible from taxable income during working life. They are a powerful optimisation tool, particularly relevant for high-income taxpayers with a high marginal tax rate. However, caution is required: withdrawing capital within three years of a buy-in triggers a tax adjustment. This three-year rule must be fully integrated into any planning strategy.

Future Perspectives

The rejection of the measure in 2026 does not exclude the possibility that a reform of the taxation of lump-sum withdrawals could be put back on the table in the future. The issue of federal state funding remains open, and the debate on fairness between annuity and capital payments is not settled. It is therefore prudent to plan withdrawals well in advance, ideally five to ten years before retirement, in order to retain sufficient flexibility should the tax framework change.

The decision to choose an annuity, a lump sum, or a combination of both goes beyond tax considerations alone: life expectancy, family situation, liquidity needs, and coverage of disability and death risks are all factors that must be considered in a personalised analysis.

Would you like to optimise your lump-sum withdrawal?

Can you Withdraw your 3rd Pillar in the Event of a Serious Illness?

In Switzerland, it is possible to withdraw your 3a pillar in certain well-defined cases. Indeed, to make an early withdrawal, the capital you wish to take from your pension must be used for one or more of the following reasons:

- You are leaving Switzerland permanently to settle in another country

- You wish to use this money for housing (purchase or construction; renting does not qualify)

- You wish to become self-employed

- You wish to use this money to fill gaps in your 2nd pillar

- You are recognized as disabled by the Disability Insurance (DI/IV).

In this article, we focus on this last case: withdrawing Pillar 3 in the context of a serious illness that leads to AD

What are the Conditions for Withdrawing your 3rd Pillar for Health Reasons?

Withdrawing your 3a Pillar

To withdraw your 3rd pillar in the case of an illness leading to disability and an inability to work, you must be receiving a full disability pension from DI (Disability Insurance). As soon as a person lives or works in Switzerland, they are automatically insured under DI.

To be considered disabled and entitled to AI benefits, you will need to submit an application via a form. It will then be reviewed, and the competent authorities will determine your entitlements.

It is therefore not the illness itself that allows the withdrawal, but rather the recognition of disability by the AI.

Withdrawing your 3b Pillar

What is Considered a Serious Illness According to the IV/AI?

For AI, disability is defined as a “reduction in the ability to earn or perform usual tasks, such as household chores, resulting from a physical, psychological, or mental health impairment.”

More often than not, it is mental health disorders that lead to an incapacity for work. Whether the incapacity is mental or physical (resulting from an accident or an illness), as long as it is long-term (at least one year), you may be considered disabled.

From that point on, the premiums waiver in the event of loss of earning capacity can step in to provide financial support.

Protection Provided by the 3rd Pillar in the Event of Disability

A 3rd pillar insurance contract allows you to cover risks such as death or disability. For example, it allows you to:

- Guarantee a pension in the event of disability

- Maintain pension benefits even in the event of an illness leading to disability

When you take out a 3rd Pillar policy, you commit to paying regular premiums. If a serious illness entitles you to IV/AI benefits and you are unable to work, paying these premiums can quickly become difficult.

The Essential Point Many People are Unaware of: Premiums Waiver

If you are recognized as disabled by Disability Insurance (DI), your premium payments are made on your behalf. You do not have to worry about this financial aspect, and your pension savings continue despite your incapacity for work.

To benefit from this option, you must pay a small additional premium each month. This amount is very low compared to the benefit you receive in the event of disability.

In other words: you pay a little more now to avoid having to continue paying your insurance premiums if one day you can no longer work and have a reduced income.

Prepare for Life's Uncertainties

Conclusion

No one is immune to a serious illness. Given the uncertainties of the future, it is always wise to be prepared. With a small additional monthly amount, add premium waiver coverage and stay protected in the event of DI (Disability Insurance) invalidity.

In brief

- Accessible to all cross-border workers employed in Switzerland with income subject to social security contributions

- Tax deduction possible only with quasi-resident status (90%: income taxed in Switzerland), cantons of Geneva and Fribourg only

- Ceiling 2026: CHF 7,258/year for employees affiliated with a pension fund

- New for 2026: Retroactive buyback of missing contributions possible

- Withdrawal: No double taxation thanks to the Franco-Swiss agreement

Why should cross-border commuters think about additional savings?

Income from 1st and 2nd pillars are not enough to maintain a standard of living after retirement, especially for those who have not worked exclusively in Switzerland. The 3rd pillar represents an essential compensation tool. In addition, it offers the possibility of investing in a variety of vehicles, some of which guarantee capital security.

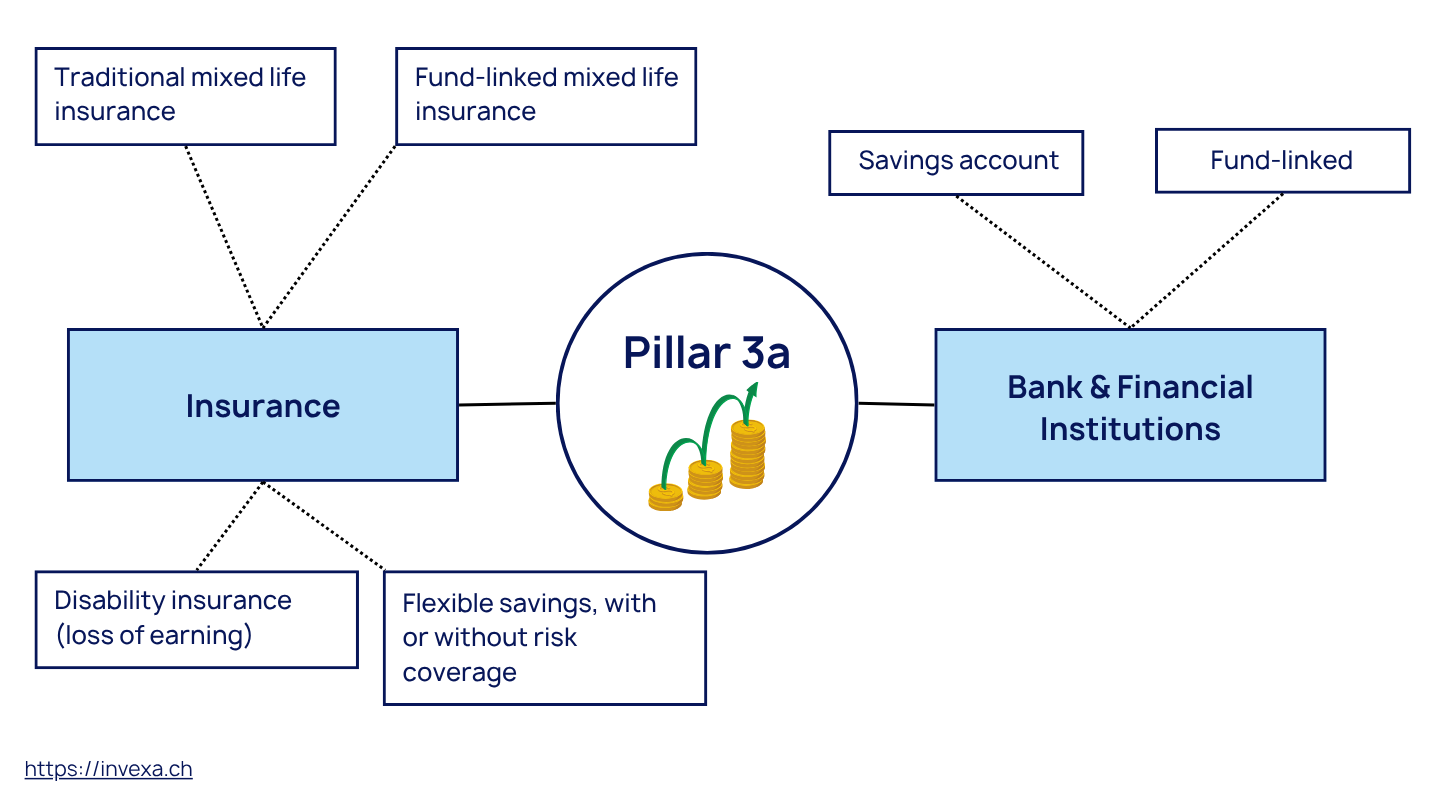

3rd pillar A or B for cross-border workers?

In Switzerland, there are two types of third-pillar pensions: the tied personal pension (3rd pillar A)and the unrestricted individual pension plan (3rd pillar B).

Pillar 3A (restricted pension plan)

The Pillar 3a is designed specifically for retirement. The funds paid into it can only be recovered at the time of retirement or under certain conditions. exceptional situations (purchase of principal residence, permanent departure from Switzerland, etc.).

Payments are deductible of taxable income, subject to compliance with certain conditions, in particular for cross-border commuters (for example, the choice of cross-border commuter status). quasi-resident in some cases).

Pillar 3a contribution limits

In 2026, it will be possible to pay out the following amounts in tied personal pension plans:

- Employees affiliated to a pension fund: Up to CHF 7,258 / year

- Self-employed or employees not affiliated to a pension fund: 20% of income, maximum CHF 36,288

Bank or insurance?

The 3rd Pillar A is divided into two categories: in banking and insurance. In insurance, we find classic life insurance (pure risk) or mixed (part of savings in funds or interest-bearing account), but also disability insurance, essential for the self-employed. Increasingly, insurance companies are also offering life insurance contracts. more flexible tied pension planssimilar to the 3a banks, but which offer covers (e.g. waiver of premiums in the event of disability, profit sharing, guarantees, etc.).

3a banking offers a more simple and flexibleThis type of account allows you to pay in the amount you want each year. Essentially, there are two possible forms: the interest-bearing account, linked to a investment funds. No additional coverage is available.

| Criteria | 3a insurance | 3a bank |

|---|---|---|

| Payment frequency | Determined in advance | Flexible |

| Type of investment | Classic (simple savings) Mixed (savings/risk) Up to 100% funds |

Classic (simple savings) Up to 100% funds |

| Surplus earnings | Profit sharing | No participation |

| Possible coverage | Deaths Disability |

No |

| Bankruptcy guarantee | Amount guaranteed to 100% | Guarantee up to CHF 100,000 |

| Waiver of premiums in the event of disability | Possible | No |

| Investment horizon | Long term only | Medium to short term |

| Share of guaranteed capital | Possible | No |

| Pledging | Possible | Possible |

| Key benefits | Insurance coverage Profit sharing Amount guarantee More safety |

Higher surrender value Best financial return Flexible payments |

What strategy should you choose in 2026? Many cross-border workers open a basic health insurance plan for social protection and top up the remaining amount of the cap (CHF 7,258) via a bank account in order to maximize returns and flexibility.

Pillar 3B (unrestricted pension plan)

Unlike the 3A, the 3B is not designed exclusively for retirement. It offers great freedom in the use of funds, which can be mobilized for a variety of projects or financial needs. When we talk about 3B, we mean all the instruments that are not included in the 1st, 2nd and 3rd pillar A. These may include life insurance, classic cars, savings accounts, stocks or bonds, real estate, or even a life insurance contract. life annuity.

Contributions are not capped, allowing everyone to adjust their savings according to their financial situation and personal objectives. 3B offers a number of tax advantages, includingtax exemption on lump-sum benefits on withdrawal (if the pension provision is fulfilled), as well as income tax of only 4% for single-premium life annuities.

Tax deductions in pillar 3b: Contributions to a pillar 3b (life insurance only) are also tax-deductible in the canton of Geneva (single person: CHF 2,345/year) and Fribourg (single person: CHF 750/year).

New for 2026: retroactive buyback

Since January 1st, 2026 (for the 2025 tax year), a major reform allows insured individuals to make up for years in which they were unable to contribute the maximum amount to their 3rd pillar. This measure is particularly beneficial for cross-border workers who started their careers in Switzerland later or who did not previously have quasi-resident status.

Key points to remember:

- Frequency: You can make a buyback every ten years.

- Deduction condition: To deduct this buyback from your taxes in 2026, you must strictly meet the conditions of quasi-resident status (90% of worldwide income taxed in Switzerland) in the year of the buyback.

- Justification: The buyback amount is limited by your pension “gap” (the difference between what you could have contributed and what you actually contributed in the past).

- Before making a large contribution, request a certificate of your past contributions from your pension provider in order to accurately calculate your buyback entitlement.

Conditions for subscribing to a 3rd pillar as a cross-border worker

For a cross-border worker, access to the 3rd pillar, particularly the tied pension plan (3a), is based on a key condition: quasi-resident status.

Quasi-resident status: the key condition

Quasi-resident status is the key that unlocks the door to tax deductions. Since the major reform of 2021, the rules have drastically changed for the 3rd pillar border in Geneva. Whereas in 2024 and 2025 Border residents had to adapt to the end of simple adjustments, the year 2026 stabilize the system while also providing the unprecedented advantage of retroactive buyouts.

The 90% rule in 2026: To be eligible, 90% of your household’s global gross income (including your spouse’s income in France, your rental income, or your dividends) must be taxable in Switzerland.

Warning regarding remote work: If you work more than 40% of your time from France (outside of specific agreements), you risk falling below the 90% threshold and losing your tax deductions.

The TOU Procedure: How to Get Deductions

- Deadline: You have until March 31 of the following year (e.g., March 31, 2027 for your 2026 income) to file the DRIS/TOU form.

- Irreversibility Once you request a TOU, you cannot go back to the current year, even if the final calculation turns out to be less advantageous than the flat-rate schedule.

- Deductible expenses: In addition to the 3rd pillar (CHF 7,258), the TOU allows you to deduct your childcare costs, alimony payments, 3b pillar contributions, and 2nd pillar (LPP) buy-ins.

To sum up, before taking out a 3rd pillar A, it is essential to check that your income from work in Switzerland is subject to contributions. AVSthat it meets the criteria for the quasi-residentin order to benefit from tax benefits. Moreover, quasi-resident status exists only in the cantons of Geneva and Fribourg.

On the other hand, a 3rd pillar B is open to all and offers a complementary savings solution without the constraints of tax status or payment ceilings, giving you the freedom to manage your portfolio for the future.

Since January 2021, cross-border workers can no longer request a correction of withholding tax through a subsequent ordinary taxation (TOU), which removes the tax deduction on their contributions. However, by obtaining quasi-resident status — conditional on 90% of the household’s income being taxed in Switzerland — it is possible to reduce taxable income by up to approximately CHF 7,258 per year per person.

Should I Contract a 3rd Pillar as a Cross-Border Worker?

The 3A pillar is above all a tax optimisation tool. It allows you to deduct the amounts paid in from your taxable income in Switzerland, making it a particularly attractive option for individuals subject to quasi-resident status (Geneva and Fribourg).

For cross-border workers employed in the cantons of Vaud, Neuchâtel, or Jura, the situation is different due to the bilateral tax agreements between Switzerland and France. In these cantons, cross-border workers are taxed in France rather than in Switzerland. They therefore do not pay withholding tax in Switzerland.

In this context, taking out a 3A pillar loses all its tax advantages.

Should I Forget about the 3A Pillar?

- Building long-term savings

- Providing a secure framework to plan your retirement

- Attractive returns depending on the chosen investment type

What 3rd Pillar Strategy to Use by Canton?

| Canton of Work | Taxation | Tax advantages of the 3a pillar | Recommended strategy |

|---|---|---|---|

| Geneva/Freiburg | Switzerland | Raised (if quasi-resident) | Pillar 3a to lower taxes |

| Other cantons | France | None (no deduction) | Pillar 3b or life insurance France |

How can I take out a 3rd pillar as a cross-border commuter?

To open a 3rd pillar A as a cross-border commuter, you must be able to provide your G permit. medical questionnaire will be requested at the time of underwriting. Some insurance companies do not ask for a medical questionnaire if the insured is sufficiently fit. young. It is therefore advisable to open a 3rd pillar A account at an early stage.

Optimise your 3rd pillar

What 3rd pillar options are available for cross-border commuters?

In Switzerland, very few insurance companies accept cross-border commuters in the 3a category. Pillar 3a bank plans are, however, accessible to cross-border commuters in most cases.

Reporting obligations in France

- The form: Tick box 8UU on your income tax return (2042) and complete appendix 3916 (Accounts held abroad).

- What to declare: The name of the institution (e.g., UBS, VIAC, Swiss Life) and the account number. Annual interest from a 3a pillar is not taxable in France as long as it remains within the pension "tunnel."

- The fine: Failing to file your tax return correctly can incur a 1500 € fine per account even if you wouldn't have paid any tax on it.

Withdrawing your 3rd Pillar as a Cross-Border Worker: How to Avoid Double Taxation?

This is the number one fear of cross-border workers: will I be taxed twice when withdrawing my 3rd pillar? Once by Switzerland, and once by France?

The short answer is: no. The Franco-Swiss tax treaty is specifically designed to prevent this double taxation. However, the mechanism operates as an advance payment of taxes. If you do not follow the proper procedures, you could indeed lose money. Here’s exactly how the taxation works upon withdrawal.

Withholding tax levied by Switzerland (advance)

When you withdraw your capital (for retirement, purchasing a primary residence, or permanent departure), Switzerland does not pay you 100% of the amount.

The pension institution (your bank or insurance company) is legally obliged to withhold a withholding tax. This is not a penalty, but a guarantee for the state.

The rate of this tax does not depend on your canton of work, but on the canton where the foundation of your 3rd pillar is domiciled. (This is why many foundations are located in cantons with favorable tax regimes, such as Schwyz).

Obligation to inform in France

As a French tax resident, your worldwide income must be declared in France. Withdrawal of your 3rd pillar is no exception. In the year following your withdrawal, you must report this capital to the French tax authorities (via forms for income received abroad, such as 2047, and the standard 2042 tax return).

France will then apply its own taxation on this capital (a flat-rate levy of 6.75% on the capital, plus social contributions CSG/CRDS).

To avoid this dreaded double taxation, the Franco-Swiss bilateral treaty allows you to recover the full withholding tax that Switzerland deducted when you withdrew your 3rd pillar.

You have a period of 3 years after the payment of your capital to claim a refund of the Swiss withholding tax. After this period, the funds are permanently lost to the Swiss tax authorities.

Conclusion: What action should you take today?

The 3rd pillar for cross-border workers is not a “standard” product. It is a strategy that must be coordinated with your canton of work, your family situation in France, and your life plans.

In 2026, with the new contribution buyback options, the opportunity for optimisation has never been stronger. Whether you choose the flexibility of a bank or the protection of an insurance policy, the key is to start early in order to benefit from compound interest.

Frequently asked questions

Yes, cross-border commuters can take out a 3rd Pillar A, even if they live in France. This savings product is open to anyone working in Switzerland.

However, the Swiss tax advantage (deduction of payments from taxable income) is only available to cross-border commuters who have opted for quasi-resident status via T.O.U. (Taxation ordinaire ultérieure), i.e. in Geneva and Fribourg only.

No, you cannot directly transfer funds to a French Retirement Savings Plan (PER). You must proceed with a lump-sum withdrawal (subject to exit tax in Switzerland and French taxation) before reinvesting.

Yes, but under conditions. Since 2021, only cross-border workers with quasi-resident status (more than 90% of their worldwide income earned in Switzerland) can deduct their 3a contributions from withholding tax. This mainly concerns workers in the cantons of Geneva and Fribourg.

The maximum deductible amount for an employee affiliated with a pension fund (2nd pillar) is CHF 7,258 per year. For self-employed individuals without a 2nd pillar, the limit is 20% of net income, up to a maximum of CHF 36,288.

Yes, but the benefit will not be tax-related in Switzerland because taxes are paid in France (according to the 1983 agreement). However, the 3rd pillar remains interesting for retirement savings, investment fund returns, and insurance coverage (death/disability), which is often more protective than in France.

You must report the existence of your account or contract each year using form 3916 (foreign accounts) and tick box 8UU on your 2042 income tax return. No tax is due on annual interest as long as the capital is not withdrawn.

Withdrawal is possible for three main reasons: reaching the legal retirement age, purchasing your primary residence (in France or Switzerland), or starting a self-employed activity.

Yes. The capital withdrawn is taxed in France, generally through a flat-rate levy of 6.75% (plus social contributions). The withholding tax deducted at source by Switzerland at the time of payment will be fully refunded once you provide proof of declaration to the French tax authorities.

The 3rd pillar supplements the 1st and 2nd pillars (AVS/AI and LPP) to maintain your standard of living in retirement.

- The pillar 3a (linked) is a locked-in savings up to 5 years before retirement, with tax benefits under certain conditions.

- The pillar 3b (free) offers greater flexibility and can be used as savings, life insurance or investment, with no payment limit.

From 2021The classic deductions linked to the 3rd pillar (and other expenses) are only possible for cross-border commuters with quasi-resident status (T.O.U), i.e. when 90 % of household income is taxed in Switzerland.

If you complete this condition, Pillar 3a contributions can be deducted from your Swiss taxable income, up to a maximum of CHF 7,258 per year in 2025. Otherwise, you won't benefit from any tax deduction, but you can still save freely in a 3b to prepare for your retirement.

3rd Pillar A funds can be withdrawn in the following ways following cases:

- Definitive departure from Switzerland,

- Transition to self-employment,

- Purchase or repayment of a main property,

- Purchase of 2nd pillar contributions,

- Retirement (up to 5 years before legal retirement age).

The withdrawal is subject to the capital benefits tax at a reduced rate. Funds from pillar 3b, on the other hand, can be freely withdrawn, subject to the conditions set out in the contract.

Thanks to the Franco-Swiss tax treaty, you do not pay tax twice. Switzerland withholds tax at source at the time of withdrawal, but you can request a full refund once you have proven that you declared it to the French tax authorities. Note: you only have 3 years to complete this procedure.

Table of main tax deductions in Neuchâtel

| Deduction | Category | Maximum amount |

|---|---|---|

| Travel expenses | Professional | ICC: max. CHF 12,000 IFD: max. CHF 3,300 Car: 70 ct/km (up to 10'000 km), 60 ct/km (10'001-20'000 km), 50 ct/km (>20'000 km) Motorcycle: 40 ct/km Light vehicles (bicycle, moped): CHF 700 |

| Meal expenses | Professional | CHF 15/day (max. CHF 3,200/year) CHF 7.50/day with employer contribution (max. CHF 1,600/year) |

| Out-of-home expenses | Professional | CHF 30/day (max. CHF 6,400/year) Reduction to CHF 7.50 for lunch if employer participates |

| Other business expenses (flat rate) | Professional | 3% of net salary IFD: min. CHF 2,000, max. CHF 4,000 |

| Continuing education and training costs | Professional | Actual costs max. CHF 12,000/year (not limited to training related to current activity) |

| Dual careers for spouses | Professional | IFD: 50% lowest net income (min. CHF 8,600, max. CHF 14,100) |

| Building maintenance - Flat-rate (built after 31.12.2013) | Housing | 10% of total rental value |

| Building maintenance - Flat-rate (built before 31.12.2013) | Housing | 20% of total rental value |

| Building maintenance - Actual costs | Housing | Energy-efficient investments, repairs, renovations, insurance, administration |

| 3rd pillar A (employee with BVG/LPP) | Pension | CHF 7,258 |

| 3rd pillar A (self-employed without BVG/LPP) | Pension | 20% net income (max. CHF 36,288) |

| 2nd pillar (BVG) purchases | Pension | Gap amounts (Please note: no further repurchases may be made within the following 3 years) |

| Health insurance premiums | Pension | ICC: Flat-rate deduction according to personal situation Single person: CHF 4,810 Married couple: CHF 9,620 Child <18 ans: 1'140 chf Young student aged 18-25: CHF 4,210 IFD: Cumulative lump-sum deduction (see guide) |

| Interest on savings capital (debt) | Pension | Deduction limited to yields (codes 3.210, 3.220, 3.240, 3.250) Married couple: CHF 300 Other taxpayers: CHF 150 |

| Private debt (mortgage interest, loans, etc.) | Pension | Deductible up to gross asset income + CHF 50,000 |

| Childcare expenses | Family | Per child <14 ans ICC: max. CHF 12,000 IFD: max. CHF 25,800 (Supporting documents required) |

| Social deductions for children | Family | Declining balance according to net income (code 6.910) Examples: Income ≤62'700 CHF: 8'600 CHF (1 child) Income ≤72'800 CHF: 17'200 CHF (2 children) Income ≤82'900 CHF: 26'800 CHF (3 children) (See complete scale in the guide) |

| Other dependents | Family | CHF 5,000 per needy person (Maintenance costs: min. CHF 6,700/year) |

| Taxpayer in school or apprenticeship | Family | CHF 3,600 (Up to the age of 25) |

| Wheelchair activity | Family | CHF 2,500 (If gainfully employed and no OASI/DI pension) |

| Orphan of mother and father | Family | CHF 8,600 (If minor, student or apprentice) |

| Social deduction for home care | Family | Amount actually received as lump-sum compensation (ICC only) |

| Maintenance payments | Family | Amount actually paid |

| Medical and sickness expenses | Health | ICC: Amount exceeding 0.5% of net income IFD: Amount exceeding 5% of net income |

| Disability-related expenses | Health | Full amount (without deductible) |

| Donations to charitable organizations | Other | ICC & IFD: min. CHF 100, max. 20% of net income (code 4.910) (Exempt legal entities with registered office in Switzerland) |

| Donations to political parties | Other | ICC: max. CHF 5,000 (Party obtaining min. 3% of the vote in cantonal elections) IFD: max. CHF 10,600 |

| Low-income deduction | Other | Decreasing amount according to situation and net income Examples (ICC only): Single person (income ≤20'300): CHF 4'100 Married couple (income ≤24'300): CHF 5'100 Single AHV/IV pensioner (income ≤24'300): CHF 9'100 (See complete scales in the guide) |

| Social deduction on wealth | Other | Declining balance according to net assets Single person (assets ≤75'000): CHF 55'000 Married couple (assets ≤125,000): CHF 105,000 (See complete scales in the guide) |

| Tax rate reduction | Other | 50% for married couples and single-parent families (Full splitting - automatic, ICC only) |

1. Deductions related to professional activity

Commuting expenses

Your daily commute to and from work is deductible, regardless of the means of transport used. The minimum distance for these expenses to be recognized is 1.5 km per trip (or 15 minutes on foot / 5 minutes by car).

Public transport : Deduct the actual cost of your annual season ticket (SBB, regional season ticket, etc.). For IFD, these costs are allowed up to a maximum of CHF 3,300.

Personal car : The canton of Neuchâtel applies a sliding scale of kilometers:

- CHF 0.60 per kilometer for the first 10,000 kilometers

- CHF 0.40 for the next 5,000 kilometers

- CHF 0.30 for surplus

Motorcycles : CHF 0.40 per kilometer Bicycle or moped (up to 50 cm³): annual flat rate of CHF 700.

Please note: if your employer provides a company car free of charge for commuting, no deduction is allowed.

Meals away from home

- Without compensation from the employer: CHF 15 per meal, max. CHF 3,200 per year

- With allowance or company canteen: CHF 7.50 per meal, max. CHF 1'600 per year

Shift or night work

If your salary certificate or an employer's certificate confirms shift or night work, you can deduct CHF 15 per day, to a maximum of CHF 3,200 per year. This deduction cannot be combined with the deduction for meal expenses.

Weekly stay outside the canton

- Without compensation from the employer: CHF 30 per day, max. CHF 6,400 per year

- With allowance or company canteen: CHF 7.50 per meal, max. CHF 1'600 per year

Other business expenses (flat rate)

- 3% of net salary, with a minimum of CHF 2'000 and a maximum of CHF 4'000

- 10% of net salary if less than CHF 20,000 per year

Expenses for secondary dependent activity

If you have a salaried activity in parallel with your main activity, you can deduct :

- ICC: 20% of net income from this activity, min. CHF 800, max. CHF 2'400

- IFD: 10% of net income from this activity, min. CHF 800, max. CHF 2'400

Dual careers for spouses

When both spouses are gainfully employed, an additional deduction is granted on the lower IFD income (after deduction of professional expenses and social security contributions): 50% of this income, with a minimum of CHF 8,600 and a maximum of CHF 14,100. At ICC, the deduction amounts to 25% of the lowest income, capped at CHF 1,200.

Training and development costs

- ICC: up to CHF 12,400 per year

- IFD: up to CHF 13,000 per year

2. Deductions for housing and buildings

Maintenance costs (for owners)

If you own a private building, you can deduct maintenance costs using one of two methods, on a per-building basis.

Flat-rate deduction :

- Property built less than 10 years ago: 10% of gross yield (ICC: max. CHF 7,200; IFD: no limit)

- Property built more than 10 years ago: 20% of gross yield (ICC: max. CHF 12,000; IFD: no limit)

Deduction of actual expenses : you deduct expenses actually incurred and invoiced during the year (repairs, renovations, administration costs, insurance, property taxes, etc.). Investments that add value to the building are not deductible under this heading, but may be partially deductible as energy-saving expenses.

Energy-efficient investments : Expenditure on improving thermal insulation or using renewable energies is fully deductible from income, including for new buildings.

Pension and insurance

Pillar 3a (tied personal pension provision)

The Pillar 3a remains one of the tax deductions the most advantageous in the Swiss system. For 2026, the deductible amounts are :

- Employees affiliated to a pension fund (LPP): max. CHF 7,258

- Self-employed without BVG: 20% of net earned income, max. CHF 36'288

For the deduction to be valid for the current year, the payment must be made before December 31.

From now on, it is also possible to make Pillar 3a purchases, This allows you to invest via a tailor-made solution while benefiting from substantial tax savings.

2nd pillar (BVG) purchases

The buying into your pension fund are fully deductible, up to the amount of the purchase potential calculated by the pension fund. This deduction is particularly attractive for high-income earners, as it significantly reduces the tax base.

Please note: if you withdraw assets from the 2nd pillar within three years of a redemption, previous deductions may be cancelled by the tax authorities.

Health, accident and life insurance premiums

Insurance premiums are deductible within the following limits (ICC / IFD):

Married persons living in the same household :

- With 2nd or 3rd pillar A contributions: CHF 4'900 (ICC) / CHF 3'700 (IFD)

- Without 2nd or 3rd pillar A contributions: CHF 6'125 (ICC) / CHF 5'550 (IFD)

Single persons :

- With 2nd or 3rd pillar A contributions: CHF 2,500 (ICC) / CHF 1,800 (IFD)

- Without 2nd or 3rd pillar A contributions: CHF 3'125 (ICC) / CHF 2'700 (IFD)

Interest liabilities (private debt)

Interest on private debts (mortgages, consumer credit, personal loans) is deductible. However, the deduction is limited to gross taxable yield on assets, plus CHF 50,000. Interest on construction loans and leasing contracts is not deductible.

Family and social deductions

Childcare expenses

- ICC: up to CHF 20,400 per child under age 14

- IFD: up to CHF 25,800 per child under 14 years of age

Deductions for dependent children

For each minor or adult child in training or education for whom you are responsible:

ICC (by age category) :

- 0 to 4 years: CHF 6,200

- 4 to 14 years: CHF 6,700

- 14 and over: CHF 8,200

IFD: CHF 6,800 regardless of the child's age

Maintenance payments

Needy dependents

If you are responsible for the maintenance of a person without resources or assets (elderly parent, adult child in training, etc.) and your assistance amounts to at least CHF 3,100, you can deduct CHF 3,100 to the ICC. For IFD, the deduction amounts to CHF 6,800.

Low-income deduction

Low-income taxpayers benefit from an additional social deduction, calculated on the basis of net income (section 6.19):

ICC:

- Married taxpayers and single-parent families: up to CHF 3,800 (reduced from CHF 48,000 net income, cancelled at CHF 67,000)

- Other taxpayers: up to CHF 2,100 (reduced from CHF 26,000, cancelled at CHF 47,000)

IFD: CHF 2,800 for married couples (no DFI deduction for single-parent families).

Health

Medical expenses

Sickness and accident costs incurred personally and not reimbursed by health insurance are deductible, but only for the portion that exceeds 5% of your net income (section 6.16 of the declaration).

The following are covered: medical consultations, dental care, glasses and contact lenses, prescription drugs, hospitalization costs, nursing home costs (less a pension portion).

Disability-related expenses

- Low income: CHF 2,500

- Average disability: CHF 5,000

- Severe disability: CHF 7,500

- Deafness or dialysis (on medical certificate): CHF 2,500

Donations and voluntary contributions

Donations to charitable organizations

Donations to tax-exempt charitable institutions domiciled in Switzerland are tax-deductible, provided the annual total is at least CHF 100 :

- ICC: up to 5% of net income (section 6.16)

- IFD: up to 20% of net income

Payments to political parties

- ICC: up to CHF 5,200

- IFD: up to CHF 10,600

Tax rate reduction (splitting)

Tips for optimizing your deductions

Keep all your receipts

Compare flat-rate and actual costs

Compare flat-rate and actual costs

For business expenses and building maintenance, systematically compare the lump-sum amount with your actual expenses. In the case of major work or costly training, actual expenses may be more advantageous.

Plan your BVG/LPP purchases and 3a payments

Spread your 2nd pillar purchases over several years to maximize the tax advantage each year. Pillar 3a contributions must be made before December 31 to be tax-deductible in that year. Plan to make Pillar 3a purchases too.

Anticipate maintenance work

Declare all your childcare expenses

Don't forget training costs

When should you file your Neuchâtel tax return?

The tax return for the 2025 tax period must be returned to the Neuchâtel Tax Department by March 31, 2026 at the latest. A request for a free extension may be granted until April 30, 2026.

An extension can be requested online via a form (individual deadline request) or via the Guichet Unique.

When should you file your Neuchâtel tax return?

The canton of Neuchâtel offers a comprehensive framework of tax deductions, covering everything from business expenses to pensions, family, health and donations. By knowing your rights and completing your tax return carefully, you can make significant savings on your annual tax bill.

If your situation is complex (multiple incomes, real estate ownership, substantial assets, self-employment), don't hesitate to consult a specialist. tax advisor to optimize your declaration.

How to take out a mortgage in Switzerland: The complete guide 2026

How to take out a mortgage

- Personal contribution : Minimum 20 % of the value of the property (including at least 10 % outside the BVG/2nd pillar).

- Borrowing capacity : Your theoretical expenses (interest at 5% + depreciation + maintenance) must not exceed 33 % of your gross annual income.

- Rate models : Choice between fixed rate (security), SARON rate (flexibility/market) or variable rate.

- Amortization : Debt must generally be reduced to 65 % (2/3 of value) within 15 years or before retirement.

- Taxation : Interest and maintenance costs are tax-deductible; indirect amortization via the 2nd or 3rd pillar allows you to optimize your taxes.

Table of contents

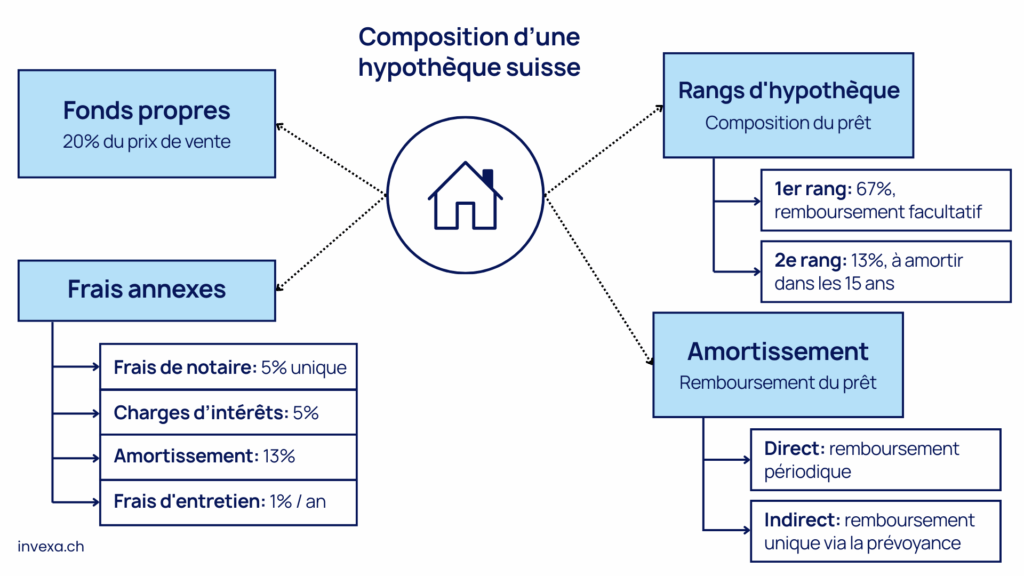

What is a mortgage?

In Switzerland, buying a property is generally done through a mortgage loanbank financing based on the pledging of the property. It's an accessible solution, but subject to strict rules. For example, banks require a down payment of at least 20 % of the property's price and assess the borrower's financial viability using the debt ratio and disposable income.

With so many offers available and so many different financing options, it's essential to understand the mechanics of mortgages to avoid the pitfalls and optimize your real estate investment.

Composition of a mortgage in Switzerland

A mortgage is made up of several key elements that define its cost, structure and repayment.

1. Borrowed capital

This is the amount that the bank or lending institution makes available to the borrower to finance the purchase of the property. In Switzerland, this amount can cover up to 80 % of the property's value, the 20 remaining % to be financed by the buyer's personal contribution.

Example For a property in CHF 1,000,000mortgage can be up to CHF 800,000with a personal contribution of CHF 200,000.

2. Mortgage interest

These are the fees the borrower pays to use the money lent. They vary according to the type of rate chosen.

- Fixed rate: stable over the entire term of the contract (2 to 15 years on average).

- Variable rate: evolves with the market, often revised every 3 to 6 months.

- SARON rate: based on the Swiss monetary rate, with frequent adjustments.

The mortgage rates are regularly updated and should be compared before making a choice.

3. Capital amortization

Amortization is the gradual repayment of borrowed capital. In Switzerland, there are two types of amortization :